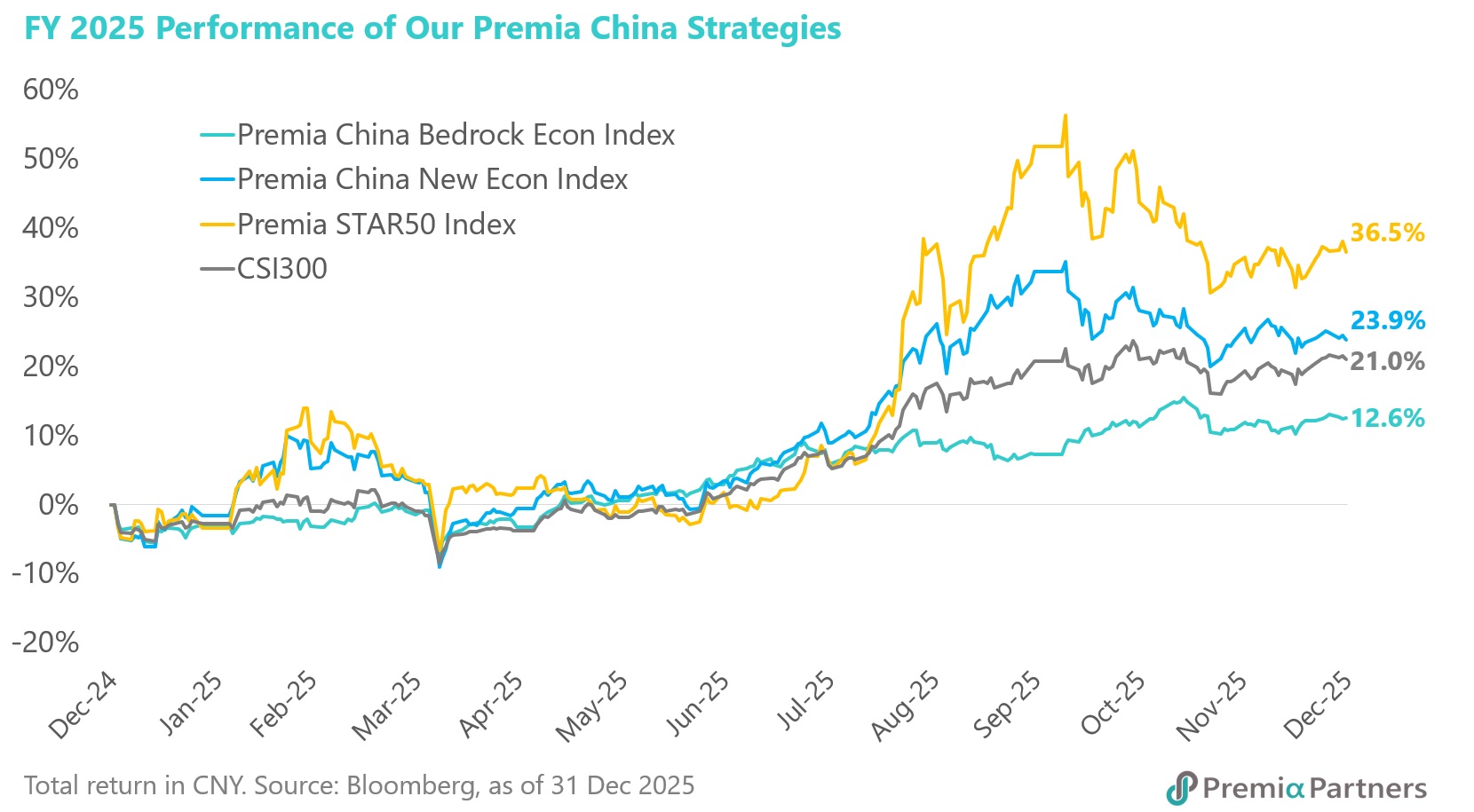

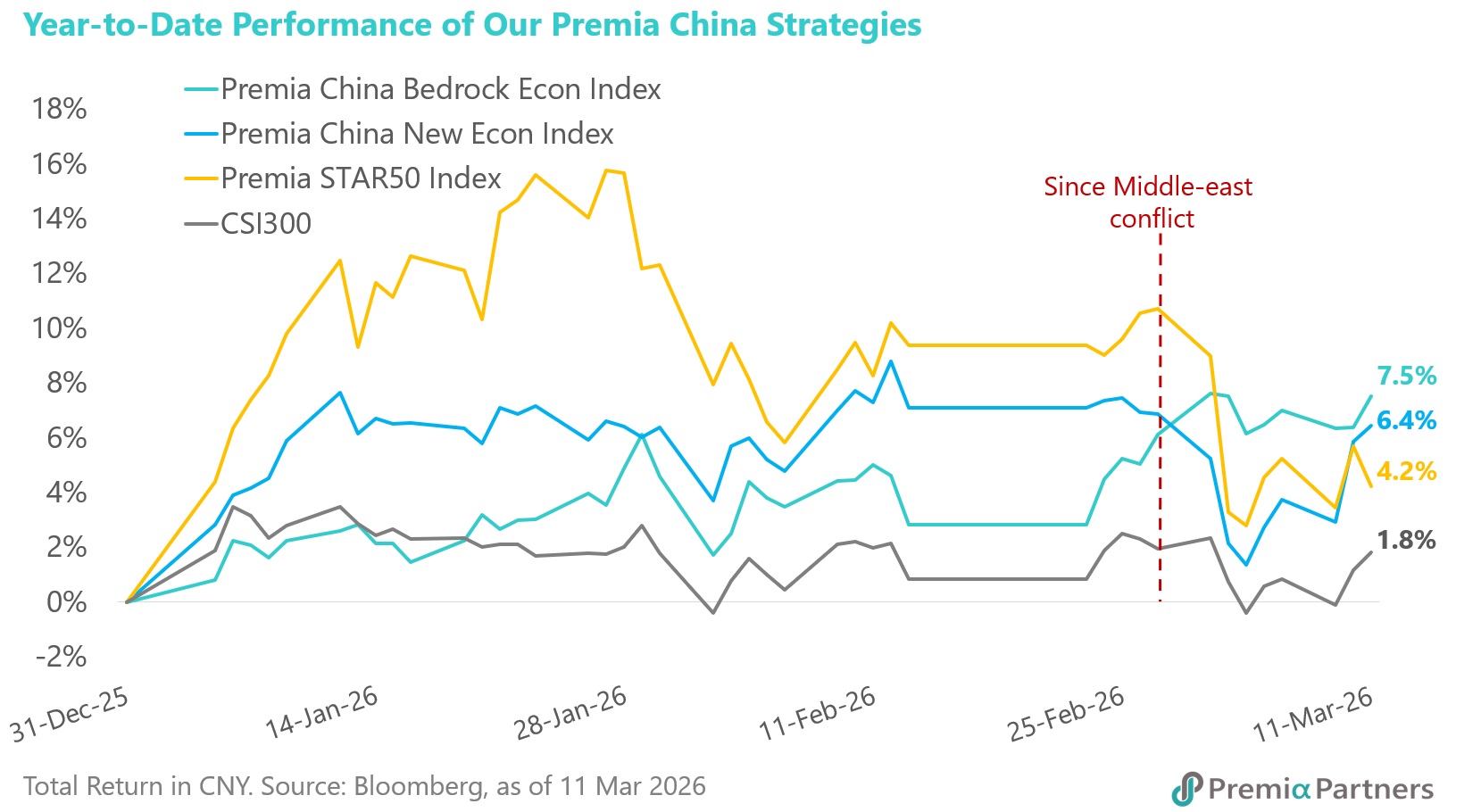

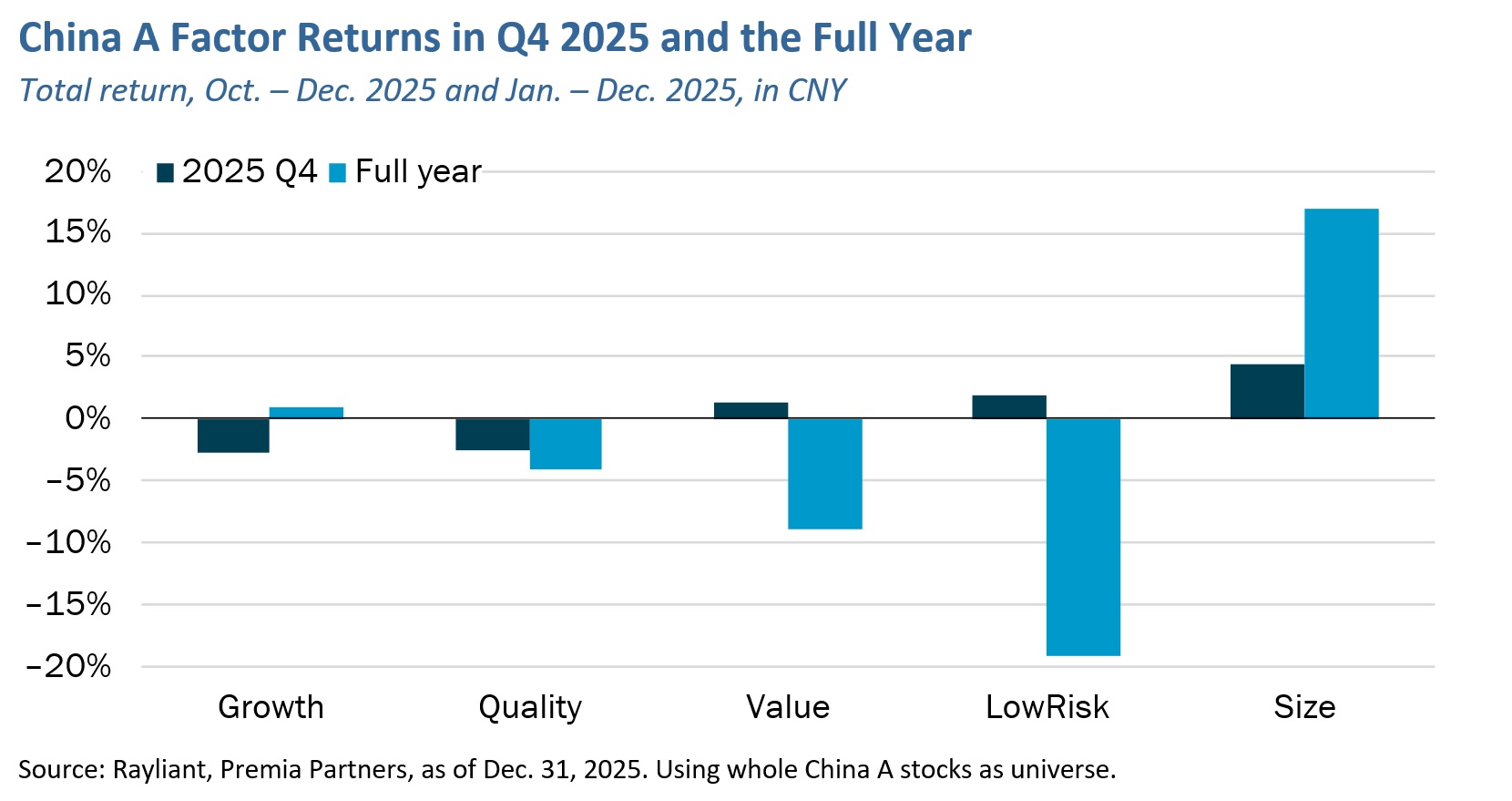

Macro Themes and Factor Performance

After a strong first nine months of 2025, Chinese equity performance was mixed in the fourth quarter, as mainland investors reevaluated their positioning and contemplated profit-taking amidst re-escalation of US-China trade frictions, including moves by Beijing to restrict access to rare earth minerals, a critical input to global technology supply chains. Meanwhile, macro data continued to bear out a familiar narrative: China’s economy has grown just fast enough to meet policymakers’ target of “around 5%” year-over-year expansion, while consumer sentiment sags, property market stress persists, and exports continue to be a primary driver of activity—albeit one that’s clearly vulnerable to those aforementioned trade risks. Given such concerns, it was little surprise to see crowded trades in the Growth space give way during Q4 to more defensive Value and Low Risk plays, as illustrated by the factor returns plotted below.

Such fourth-quarter Growth-to-Value rotation contrasted, of course, with dynamics over the prior three quarters, when a technology-driven equity bull market in mainland Chinese stocks led the Growth theme to strongly outperform Low Risk and Value factors, the two poorest exposures depicted above. Throughout the year and in the final few months of 2025, small-cap stocks remained relative winners, reflecting more clearly the technology and high-value manufacturing that has been at the heart of improving growth expectations for China’s economy, but also a swath of the market more susceptible to powerful retail investor sentiment and a subset of firms thought to be less at risk in the face of trade policy uncertainty—and possibly more likely to receive support from Beijing in the event such difficulties do arise.

Comments on Index Performance in Q4

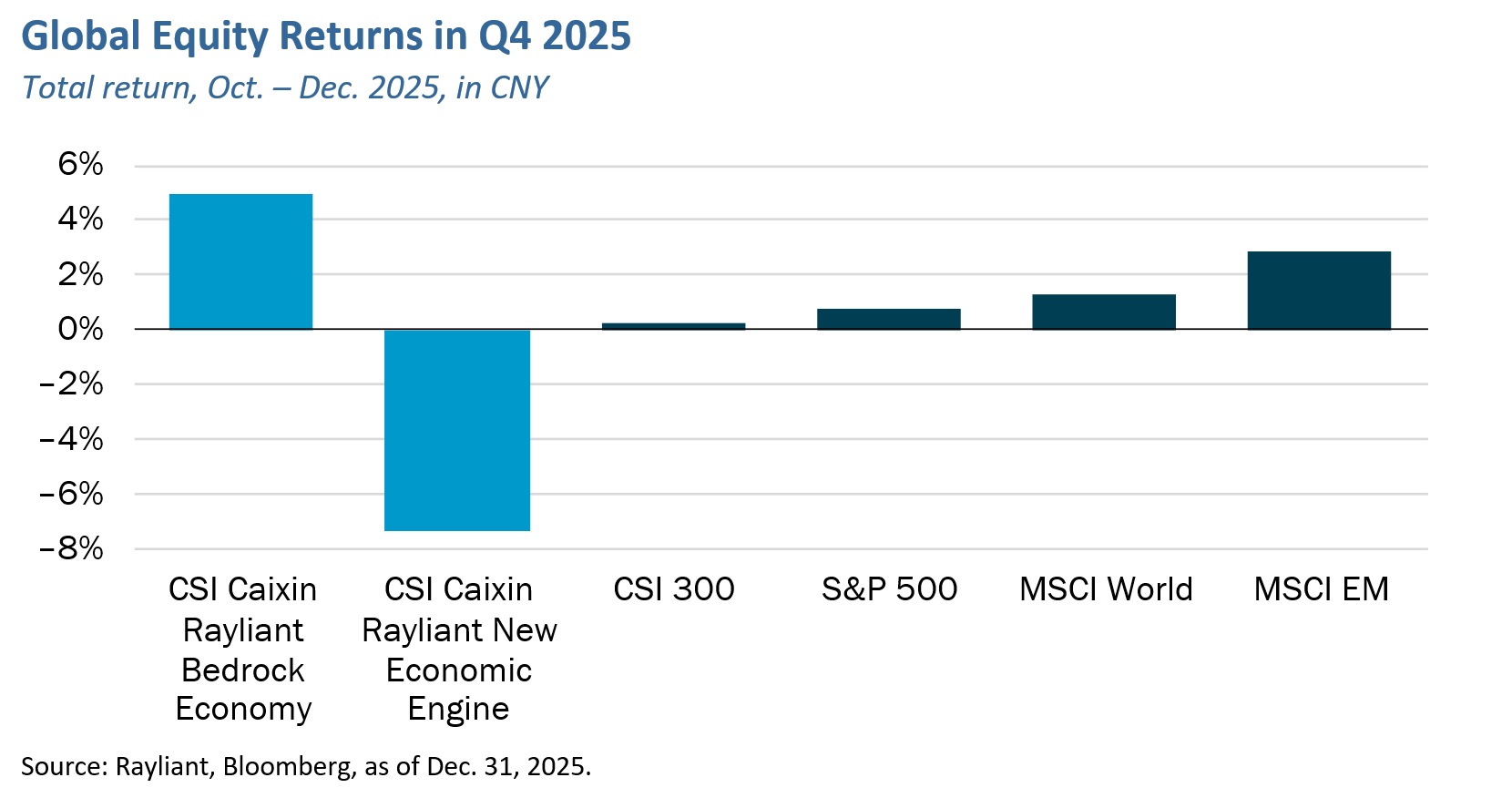

As mentioned, amidst profit-taking pressure and greater macro uncertainty in Q4, Chinese equities treaded water heading into the end of 2025, with the CSI 300 Index rising by just 0.2% (CNY) over the three months ending December 31st, 2025, as shown below. US stocks likewise posted modest gains of 0.7% (CNY) in Q4, as equity investors climbed a “wall of worry”, bucking concerns over seemingly stretched stock valuations—particularly in the tech sector—continued trade policy uncertainty, geopolitical threats, and the Trump administration’s pressure on the Fed to accelerate rate cuts. Turning to broader emerging markets, performance was much stronger, as South Korea returned over 27% for the quarter—and similarly Taiwan rallied amidst continued strength in the AI theme and their unique strategic roles in the global semiconductor supply chain. Optimism that tariff threats earlier in the year would give way to dealmaking, as well as Fed rate cuts at each of the central bank’s last three meetings of the 2025 provided further tailwinds to EM stocks.

The factor rotation from Growth to Value mentioned above was clearly on display in terms of the Bedrock and New Economy strategies, with the CSI Caixin Rayliant Bedrock Economy Index (tracked by Premia’s 2803 HK/9803 HK ETFs) gaining 4.9% (CNY) in Q4, and the the CSI Caixin Rayliant New Economic Engine Index (tracked by Premia’s 3173 HK/9173 HK ETFs) declining by 7.4% (CNY) in the final three months of the year after strong rallies since the summer. From a sector standpoint—again, in line with that ‘factor rotation’ theme—the Bedrock strategy benefited most in Q4 from allocation decisions, including overweights to more value-oriented sectors like Materials, Energy, and Financials, and underweights to more growth-oriented sectors like Information Technology and Health Care. Selection was strongest among Financials, Industrials, and Consumer Discretionary stocks, offsetting weaker performance of picks within the Energy and Materials sectors. Likewise, the New Economy strategy suffered from an overweight to Health Care/ biotech which retreated after outperformance previous months, and underweights to Financials and Materials as investors piled in bets for precious metals and dividend strategies. Meanwhile profit-taking in Information Technology after the strong run in preceding months presented additional detraction for the quarter.

Looking ahead, as China kicks off 2026 as the first year of the 15th Five Year Plan, policy tailwinds and earnings growth would continue to provide important insights into the winners and losers for especially strategic growth sectors that China New Economy and STAR 50 focus on, while for as long as geopolitical tension and tariff risks persist, the defensive factors of low volatility and value that China Bedrock focus on would shine during windows of volatility and provide the much needed diversification in a world where investors hold the same concentrated bets.

*****************************************************************************************************

Dr. Phillip Wool is the Global Head of Research of Rayliant Global Advisors. Phillip conducts research in support of Rayliant’s products, with a focus on quantitative approaches to asset allocation and return predictability within asset classes, as well as the design of equity strategies tailored to emerging markets, including Chinese A shares. Prior to joining Rayliant, Phillip was an assistant professor of Finance at the State University of New York in Buffalo, where he pursued research on quantitative trading strategies and investor behaviour, and taught investment management. Before that, he worked as a research analyst covering alternative investments for Hammond Associates, an institutional fund consultant. Phillip received a BA in economics and a BSBA in finance and accounting from Washington University in St. Louis, and earned his Ph.D. in finance from UCLA, where his research focused on the portfolio holdings and trading activity of mutual fund managers and activist investors. Premia CSI Caixin China New Economy ETF and Premia CSI Caixin China Bedrock Economy ETF track the CSI Caixin Rayliant New Economic Engine Index and CSI Caixin Rayliant Bedrock Economy Index respectively.