The oil shock is hitting the US and Asia equities markets with heightened volatility, but their bond markets are reacting in opposite directions — and that split is where fixed income positioning have been playing out.

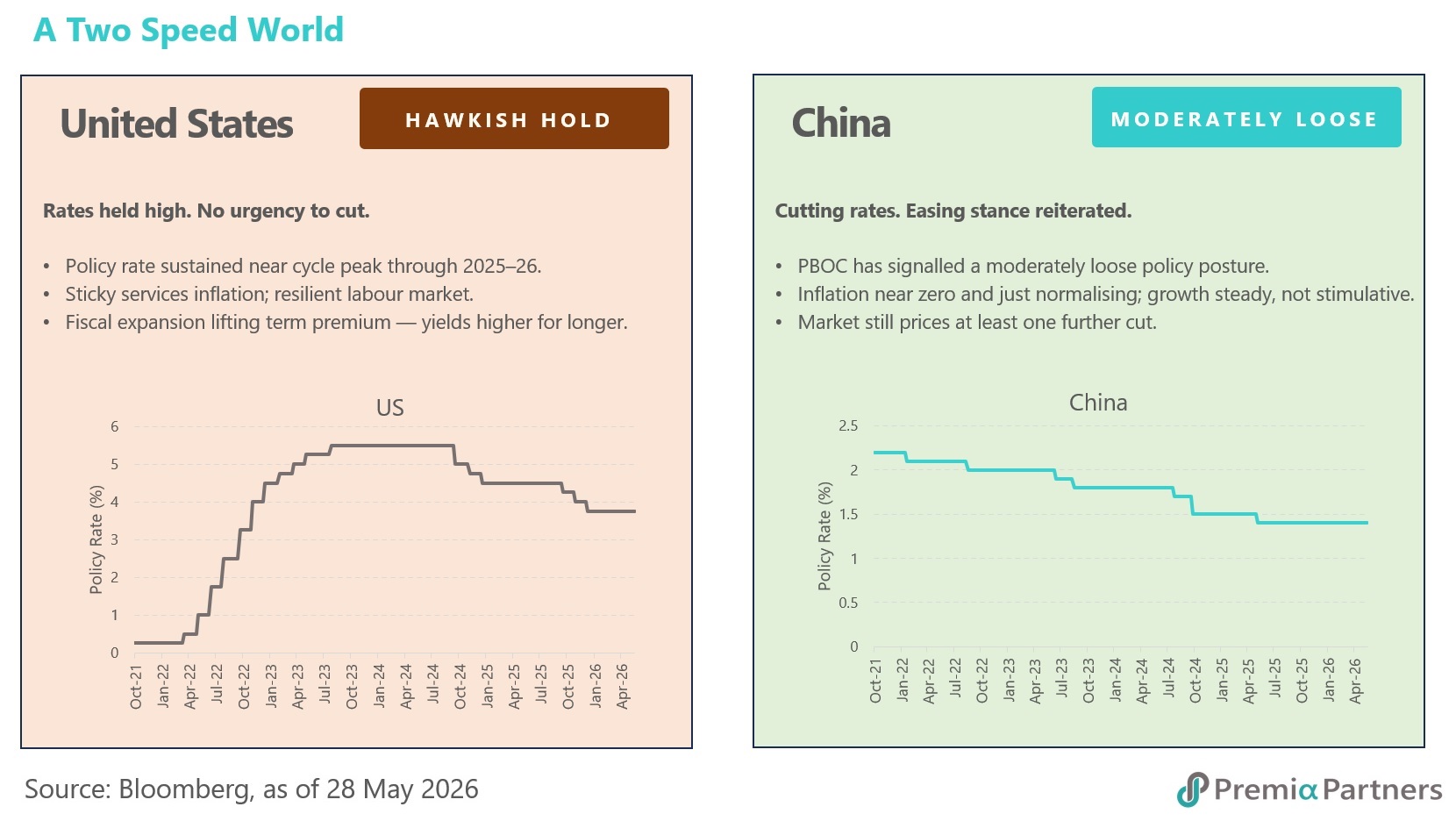

In the US, the inflationary pass-through has been fast and forceful—CPI at 3.8% year on year and PPI at 6.0%—leaving a constrained Fed under new Chair Kevin Walsh closer to hikes than cuts. The result is a rates market where the safe-haven premium has eroded, long-end yields have pushed toward 5%, and near-term easing is off the table.

Asia faces the same shock but a very different transmission. Initially seen as most exposed to a prolonged Strait of Hormuz closure given its Gulf reliance, the region has defied those fears with resilience. Outside China, economies have re-sourced imports—daily tanker data show May energy flows into Asia markets almost back to normal—aided by reserve drawdowns and a shift toward coal and biofuels. China stands apart, lower Gulf dependence and a still recovering property market keep its monetary backdrop supportive. With strong supply chain resilience and growth momentum behind it, the regional growth hit has been smaller than feared.

That resilience has set up a fragmented policy landscape. The US offers high but volatile yields with little near-term relief, while Asia spans the spectrum: hawkish tightening (the Philippines, Indonesia, Korea), patient holds (India, Thailand, Malaysia, Singapore), and a Chinese market still benefitting from accommodative conditions. This mix of US-Asia divergence and intra-Asia dispersion makes a modular, region/country-aware approach to fixed income worth considering rather than treating it as a single bloc. With this backdrop, Premia fixed income ETF range compares well with peers, separating high-quality duration, liquidity and selective carry.

High Quality Duration in China Rates

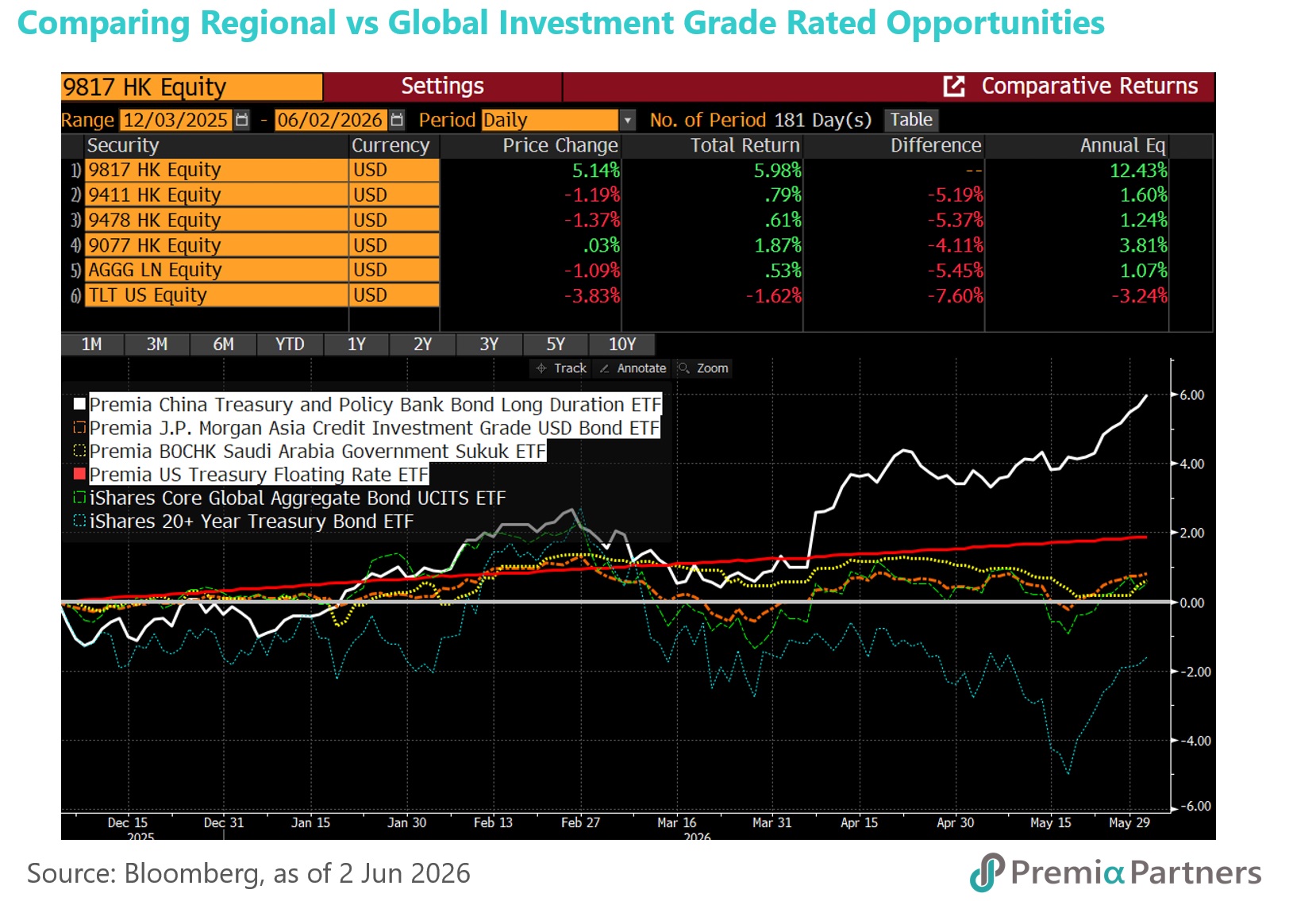

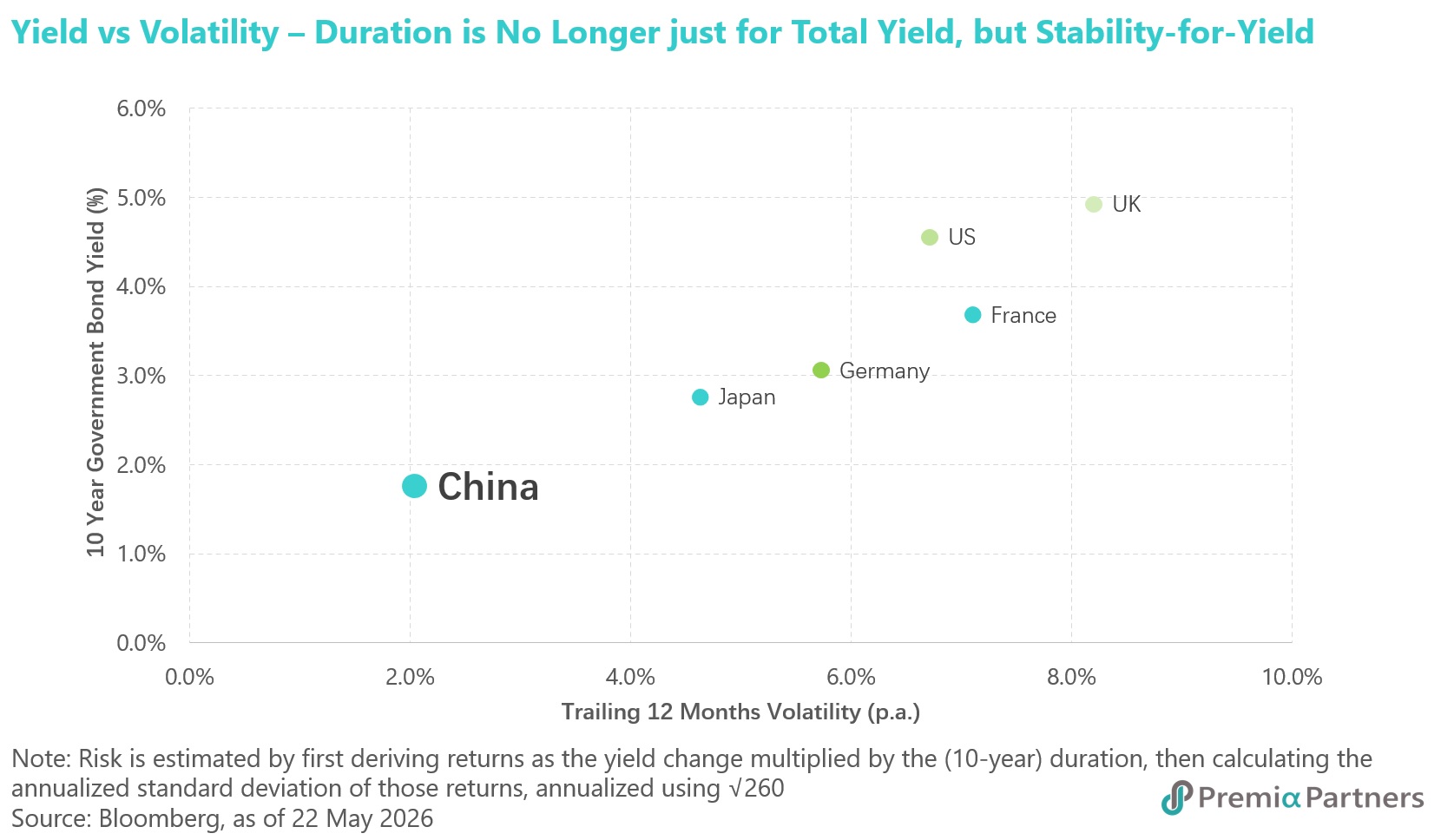

Long duration China government bonds (CGB) in particular emerged as a haven from soaring energy prices and rising global inflation, given favourable RMB movements, accommodative liquidity environment and consistent policy trend under contained inflation backdrop; in contrast to the constrained Fed and unstable US Treasury curve. Meanwhile major central banks of Europe and Japan are also under pressure to keep interest rates at higher levels than previously expected to counter inflation triggered by prolonged closure of the Strait of Hormuz.

This is why CGBs ranking among the best-performing sovereigns YTD at +6.4% in USD terms (as of Jun 2, 2026), supported by billions of foreign inflows and a Moody's outlook upgrade to Stable.

Premia’s China Treasury & Policy Bank Bond Long Duration ETF (2817 / 9817 HK) provides exposure to a basket of China government and policy bank bonds with tenors of 10 years or more, with average credit quality of A, effective duration of 17.96 years, and yield to maturity of about 2.19% (as of Jun 2, 2026).

For investors seeking to diversify away from US duration risk while maintaining a high-quality duration anchor, this ETF can serve as a structural core allocation. The case is strengthened by the fact that long-duration Chinese government bonds have continued to perform despite stronger growth and reflation signals 2026 YTD, supported by geopolitical safe-haven inflows, proactive domestic liquidity management, and an appreciating RMB. For investors concerned about renminbi volatility, the strategy is also available in a USD-hedged version (9177 HK) which benefits from the higher hedge carry due to the widened rate differential between CGB-UST 10 Year.

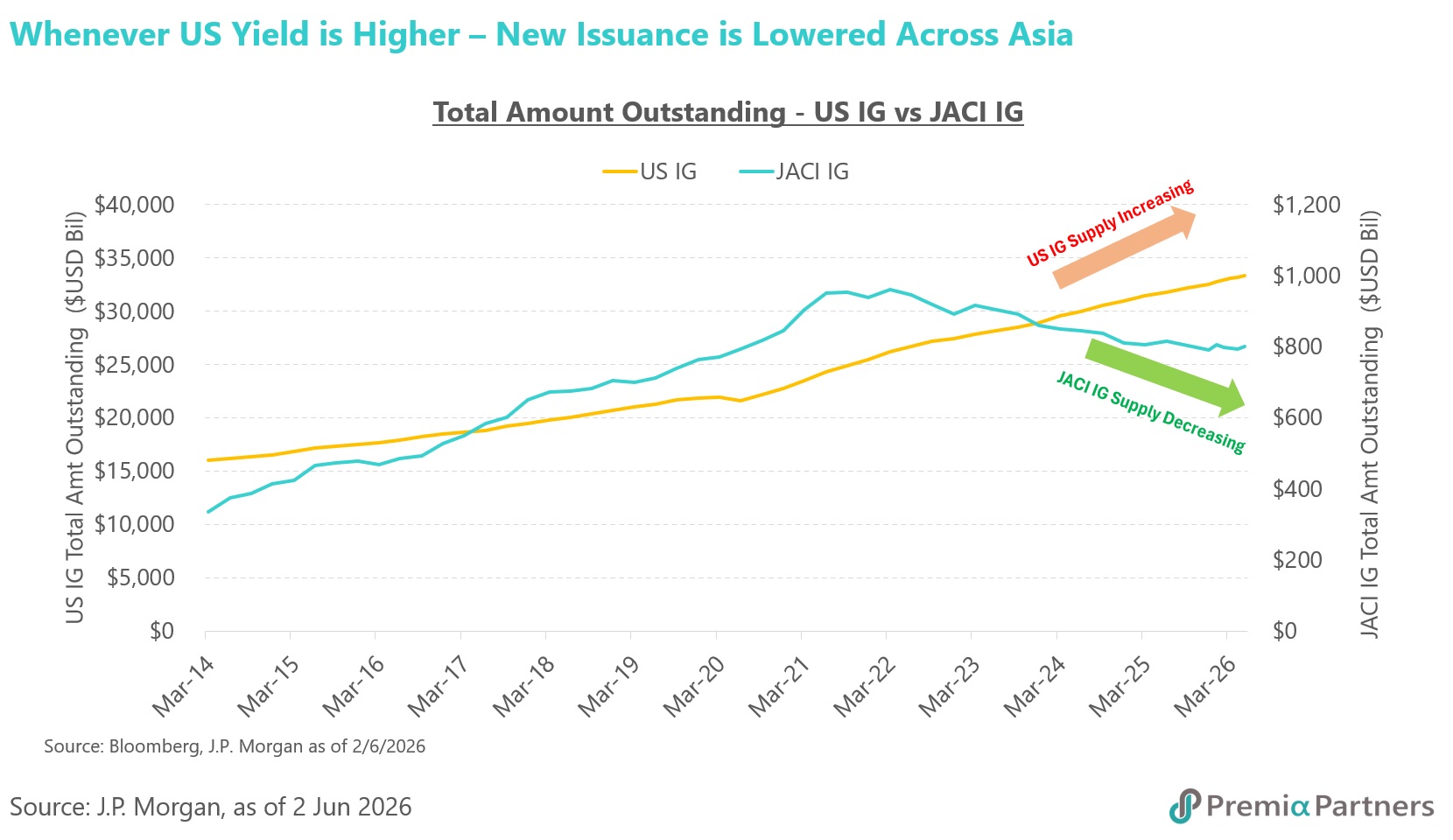

For USD based investors, a defining macro theme right now is the persistence of energy-driven inflation and the degree to which oil remains central to the global rates story. It affects US IG, Asia USD investment grade (IG) credits and Saudi Arabia sovereign sukuk in a different light, due to very different technicals and fundamentals.

Same dollar curve, opposite supply stories - US IG issuance continues to expand on the back of sustained funding needs from US hyperscaler, while the Asia USD IG universe keeps shrinking as domestic firms increasingly issue in local currency. The largest countries’ issuers in the JACI index - China, Indonesia, the Philippines, Malaysia - have all articulated measures to reduce reliance on foreign-currency issuance, whether at national level or corporate level. This tightening of net USD supply provides a structural tailwind buffer for outstanding Asia USD IG bonds prices. Meanwhile, Asia USD IG universe has long been underpinned by the same strong local investors base, and that domestic demand remains as robust as ever. The resulting supply-demand imbalance provides a supportive floor under Asia USD IG bonds, with scarce new issuance meeting firm regional demand and helping keep spreads relatively tight even as global yields reprice higher.

The technical story is also being reinforced by improving fundamentals. From the recent 2026 J.P. Morgan Asia Credit Conference, one of the panelists shared that default expectations for Asia credit have been revised down from around 2% at the start of the year to 1.8%, while year-to-date realized defaults stand at only around 0.2%. That combination of falling default risk and firm domestic demand suggests the current spread tightness rests on more than scarcity alone.

Premia J.P. Morgan Asia Investment Grade Credit USD Bond ETF (3411/9411 HK) offers diversified access to this theme through a portfolio of Asia USD investment-grade credit, with an average credit quality of A, effective duration of roughly 4.71 years, and a yield to maturity around 4.74% (as of Jun 2, 2026).

Saudi sukuk hold up either way: higher oil strengthens the fiscal position and compresses spreads, while lower oil eases inflation and pulls yields down — a roughly symmetric profile rather than a one-directional crude bet. With crude at the center of the global rates story for 2H 2026, that resilience is what turns the macro backdrop into a portfolio advantage.

On the path forward, market analysts expect oil to average around US$100 per barrel through the end of 2026 as depleted inventories keep the market tight, with the potential for prices to fall materially into 2027 should the Strait of Hormuz reopen and Gulf exporters move to restore volumes. What makes Saudi sukuk particularly interesting is that the credit tends to be supported across both legs of that path. When oil prices are higher, the Kingdom's fiscal position strengthens and spreads compress. When oil prices are lower, inflation pressure eases and yields fall, and that relief may help the broader spread market turn more risk-on, which is also constructive for spreads. This relatively symmetric profile gives the allocation a degree of resilience to the oil outlook rather than a one-directional bet on higher crude.

Furthermore, following recent developments reinforces the technical backdrop. Firstly, Saudi NDMC has already secured ~90% of its 2026 international bond funding needs, and the debt office has selectively scaled back SAR denominated issuance in May to SAR2.42bn — limited supply that puts a natural floor under spreads. Secondly, oil prices holding above the Kingdom's fiscal breakeven level (~US$90 per barrel) keep the credit outlook firmly supported. Thirdly, Saudi Arabia’s SAR-denominated sukuk will be included by two global flagship EM local-currency flagship index: Bloomberg EMLCTRUU (confirmed 23 April, 1.9% proforma weight, implementing April-end 2027) and JPMorgan GBI-EM (confirmed 22 April, 2.52% terminal weight, expected to start phasing-in from 29 January 2027). Together they anchor a structural passive-demand tailwind for SAR sukuk into early 2027, and we are just 6 months away from 2027.

For portfolio construction, this gives Saudi sukuk a dual role: a higher-yielding sovereign sleeve that diversifies away from US Treasuries, and a way to express the Middle East macro theme without relying on commodity-linked equities. It sits naturally between core government duration and higher-risk credit satellites. For investors who want fixed income exposure that is more directly aligned with that theme, Premia BOCHK Saudi Arabia Government Sukuk ETF (3478/9478 HK) offers a differentiated sovereign carry allocation, with a yield of 5.13% and duration of 5.16 years (as of Jun 2, 2026).

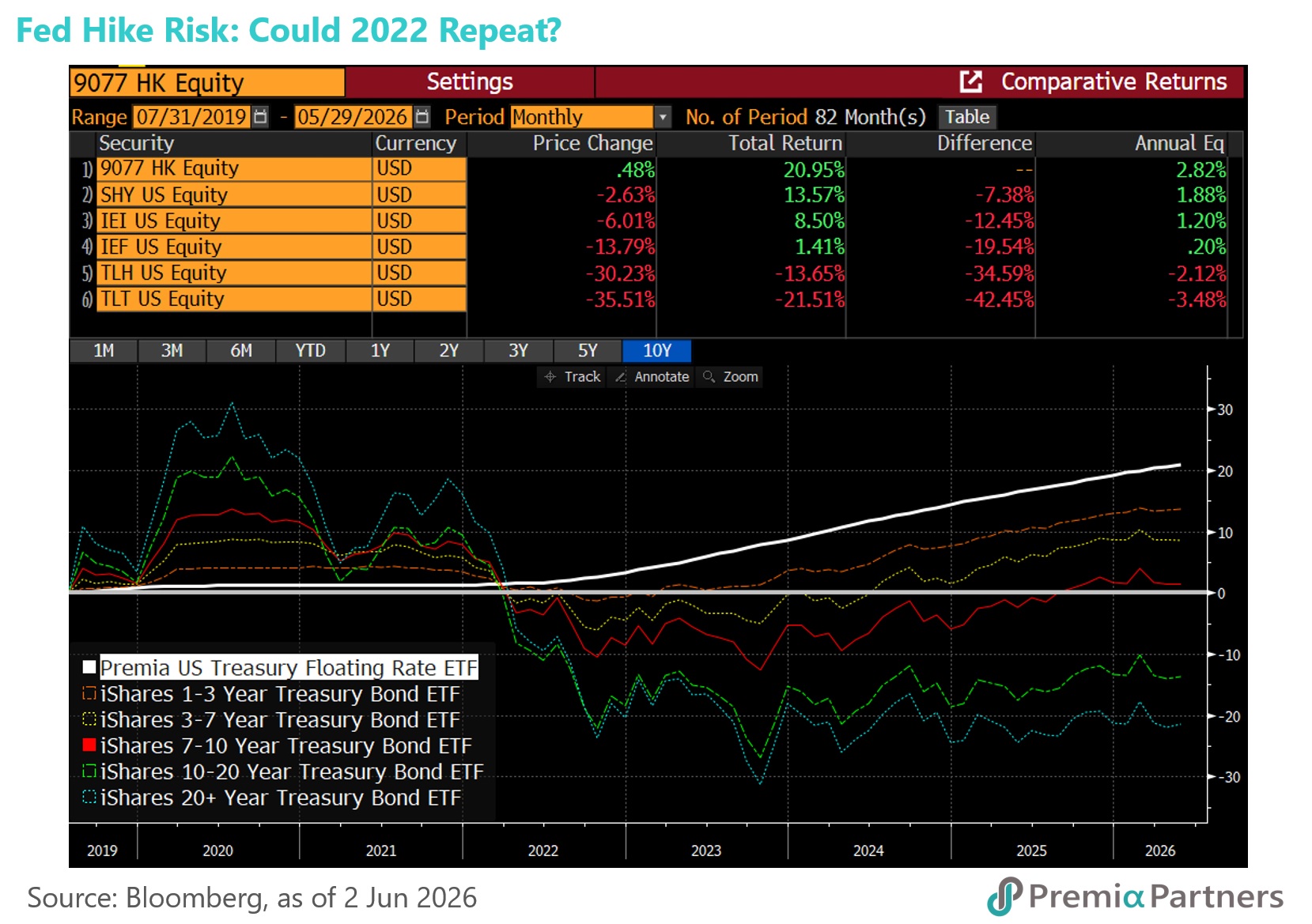

Liquidity Sleeve in US Treasury FRNs

With the hawkish Fed pivot, the macro message on the US is clear - duration risk in Treasuries is no longer an uncomplicated defensive trade. In this environment, Premia’s US Treasury Floating Rate ETF (3077/9077/9078 HK) provides a more stable way to hold liquidity inside a fixed income portfolio. The ETF underlying is a basket of US Government Treasury Floating Rate Bond with and a yield of 3.68% (as of Jun 2, 2026) with minimal duration risk.

The case for holding liquidity here is reinforced by where rates are likely to settle. While US long-end yields have at times pushed toward 5%, the prevailing market view is for the Fed to lose its easing bias and move toward neutrality, leaving the 10-year US Treasury yield anchored closer to 4.5% into year-end, with long-end yields seen drifting toward 4.2% in 2026 and 4.0% in 2027. A path that keeps the front end elevated while long-end relief stays gradual favours an instrument that resets with short duration rather than one exposed to long-duration repricing.

If the Fed is forced to remain hawkish for longer, or if inflation pressures push short-end expectations higher again, FRNs can continue to reset upward without exposing investors to the capital volatility associated with long-duration Treasuries. That makes the ETF a useful source of dry powder and a defensive buffer against a more volatile US macro path.

Selective High Yield Risk through survivor cohorts in China Property

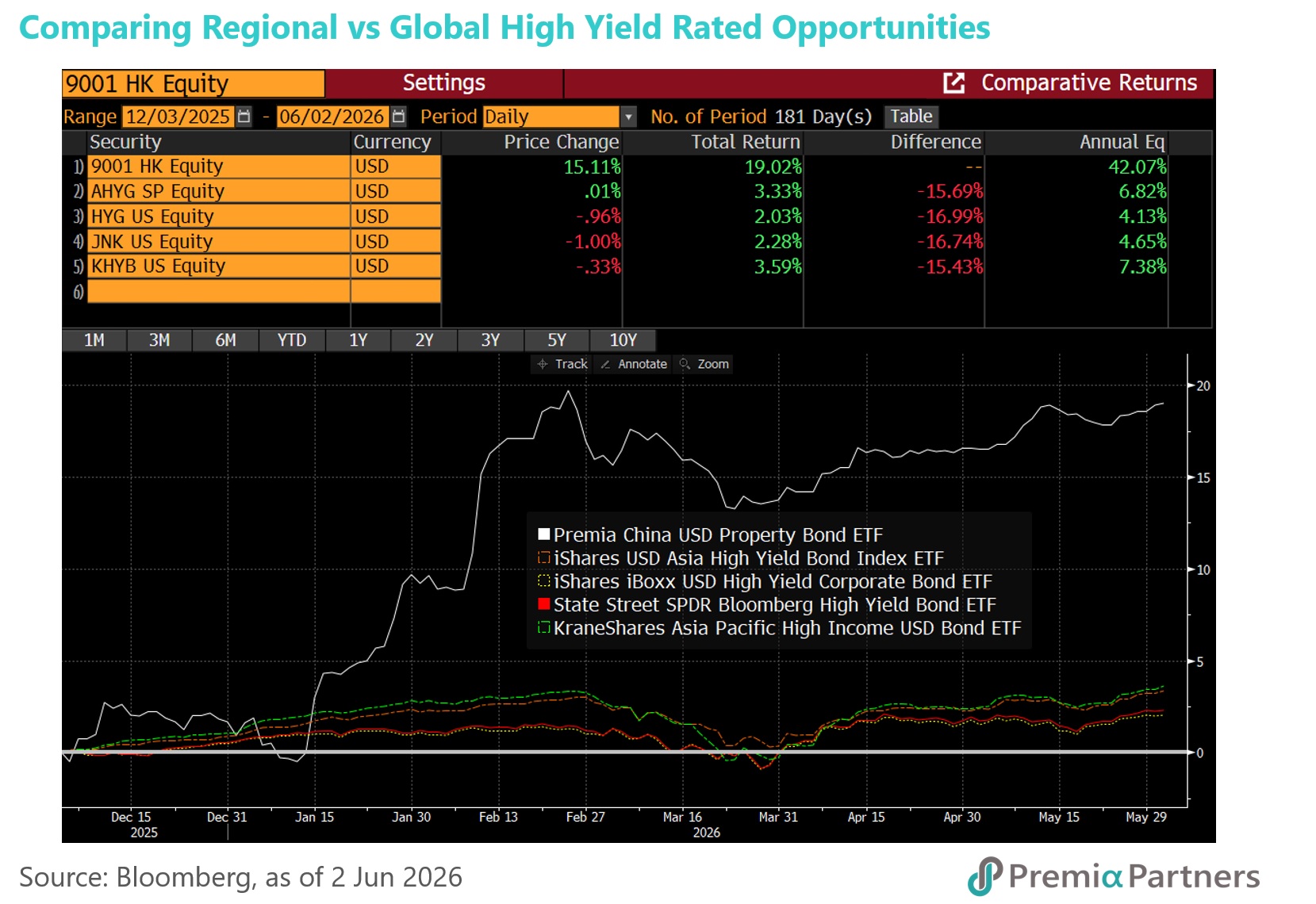

Asia high yield is no longer broadly cheap, but dispersion has increased and selective opportunities remain in segments where markets have already absorbed several years of restructuring and distress. China property is the clearest example: an extended default and restructuring cycle has weeded out the weakest issuers, leaving a cohort of stronger survivors – better capitalised, with continued funding access and policy backing – even though the sector as a whole still carries meaningful risk. Analysts including Goldman, UBS and Citi expected the property markets in Tier 1 cities to start bottoming out or narrowing gap by the end of 2026 into 2027.

The technical backdrop reinforces this. The high yield universe has shrunk and offshore developer issuance remains far below pre crisis levels, while policy easing, inventory normalisation and improving confidence in stronger names such as China Overseas Land, Yuexiu and Vanke point to more demand chasing a smaller bond pool. Against this backdrop, the China property segment – proxied by the tracking index of Premia China USD Property Bond ETF (3001/9001 HK) – continues to offer a substantial spread premium, on the order of roughly 600–700 bps above the broader USD high yield universe, even after years of price recovery. That premium remains elevated as the downturn enters its fifth year, while policy support and stabilising transactions and prices, led by tier 1 cities, increasingly underpin this stronger surviving cohort. The result is a fund offering a 13.62% yield to maturity with just 2.11 years of duration (as of 2 June 2026), so the case is now twofold: investors hold a cleaner, fundamentally stronger group of survivors and are paid an elevated spread for the residual restructuring and macro uncertainty.

For investors willing to take measured satellite risk, the ETF is a liquid, diversified way to express the view that parts of China property credit are shifting from distress toward gradual normalisation – supported by policy easing, inventory reduction and improving transaction trends. Concentration and event risk remain, so it is a satellite rather than core holding, but the tailwinds increasingly favour the stronger surviving names.

Putting it together

Taken together, the Premia fixed income lineup allows investors to build a more robust bond allocation around today’s fragmented macro regime. China duration can serve as the policy-supported duration core, Asia IG and Saudi Sukuk can provide diversified spread carry and a tactical angle to higher oil prices, US Treasury FRNs can preserve liquidity without heavy duration exposure, and China property can help investor deliver higher yield in an asset that is shielded from US macro uncertainty, with onshore property market recovery as main driver to spread compression.