Macro Themes and Factor Performance

Investors following the action in global stocks over the last few months will be acutely aware of the degree to which the markets’ fortunes turned in Q1 on developments in the Middle East. Geopolitical conditions were already tense in the preceding months, to be sure, such that late-February airstrikes by the US and Israel against Iranian targets—including the assassination of the country’s Supreme Leader Ali Khamenei—delivered a sharp jolt to shares that had run up significantly in the year prior. The sell-off was exacerbated by Iran’s response, closing off the Strait of Hormuz, through which a substantial share of the world’s oil transits on its way to big buyers in Asia.

Onshore Chinese stocks had traded up in January and February, but gave all of that back and then some as sentiment turned negative in March. While we see China’s economy as more robust to energy shocks than some of the world’s other large net oil importers—not least because of the country’s edge in new energy technology, to which Bedrock and New Economy strategies offer exposure—it was almost unavoidable that A shares would be dragged down by general geopolitical risk aversion, more specific concerns around demand-side effects of an energy price shock, as well as fears of a delay in the Fed’s timetable for monetary easing. Increasing angst around the potential disruptive implications of AI, especially among software stocks, contributed to some volatility within the technology theme.

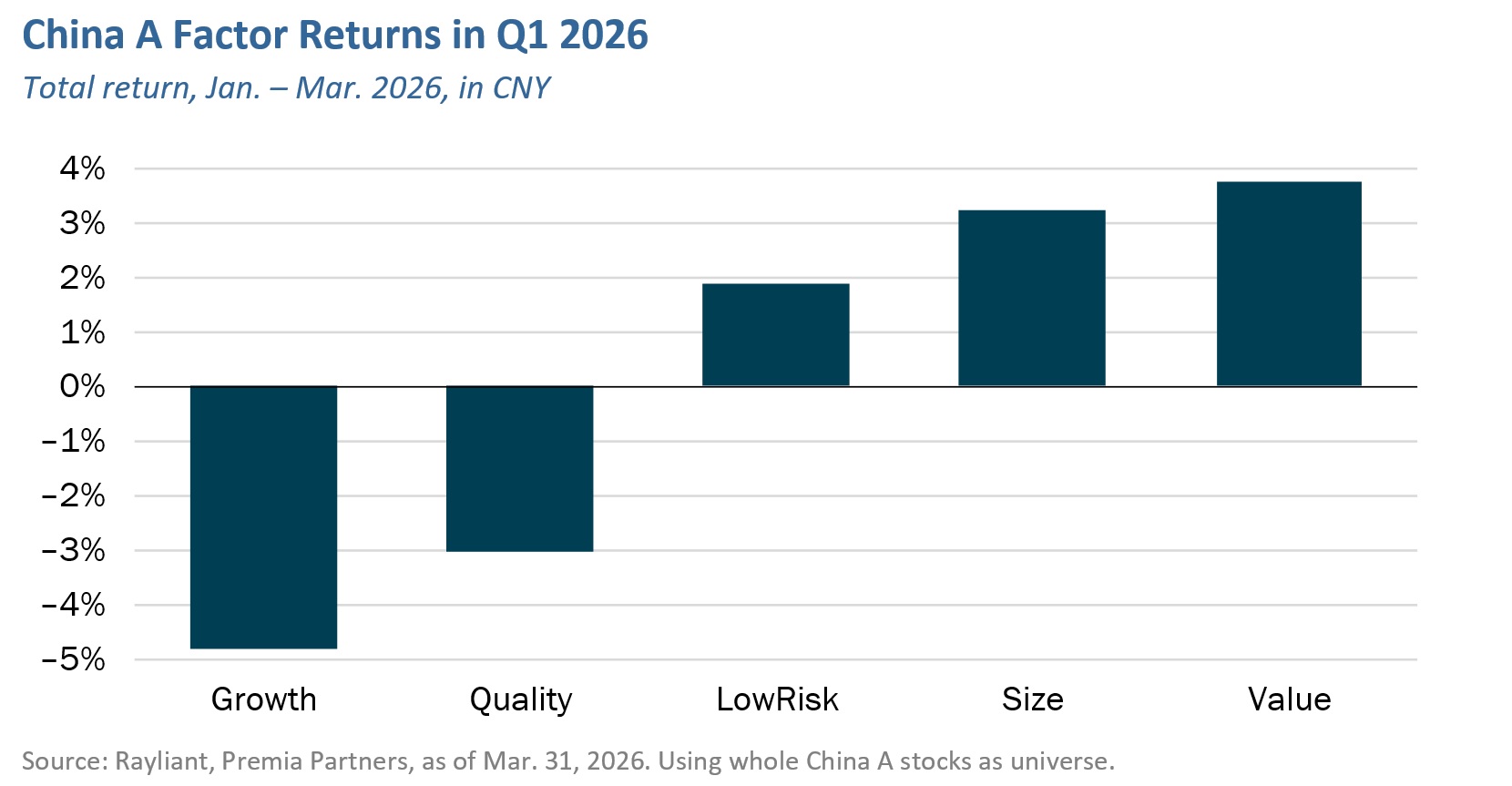

Taking our analysis to the factor level, recall that in last quarter’s commentary, we discussed a rotation underway among factor exposures, with Growth leadership giving way to Value outperformance, as profit-taking and a more defensive mindset among investors took hold. That trend continued in the first few months of 2026, with Growth and Quality factors delivering another down quarter, while Low Risk and Value flourished. Not surprisingly, the vast majority of returns to those latter two factors arose in the month of March, as pessimism around war in the Middle East stoked a rally in factors that tend to do best when investors see the macroeconomic glass as half-empty. Likewise, small-cap stocks continued to show relative strength, driven by enthusiasm toward AI adoption, positive retail investor sentiment, and—one imagines—an expectation Beijing will extend policy support to smaller stocks in the event Middle East risk bleeds into onshore companies’ fundamentals.

Comments on Index Performance in Q1

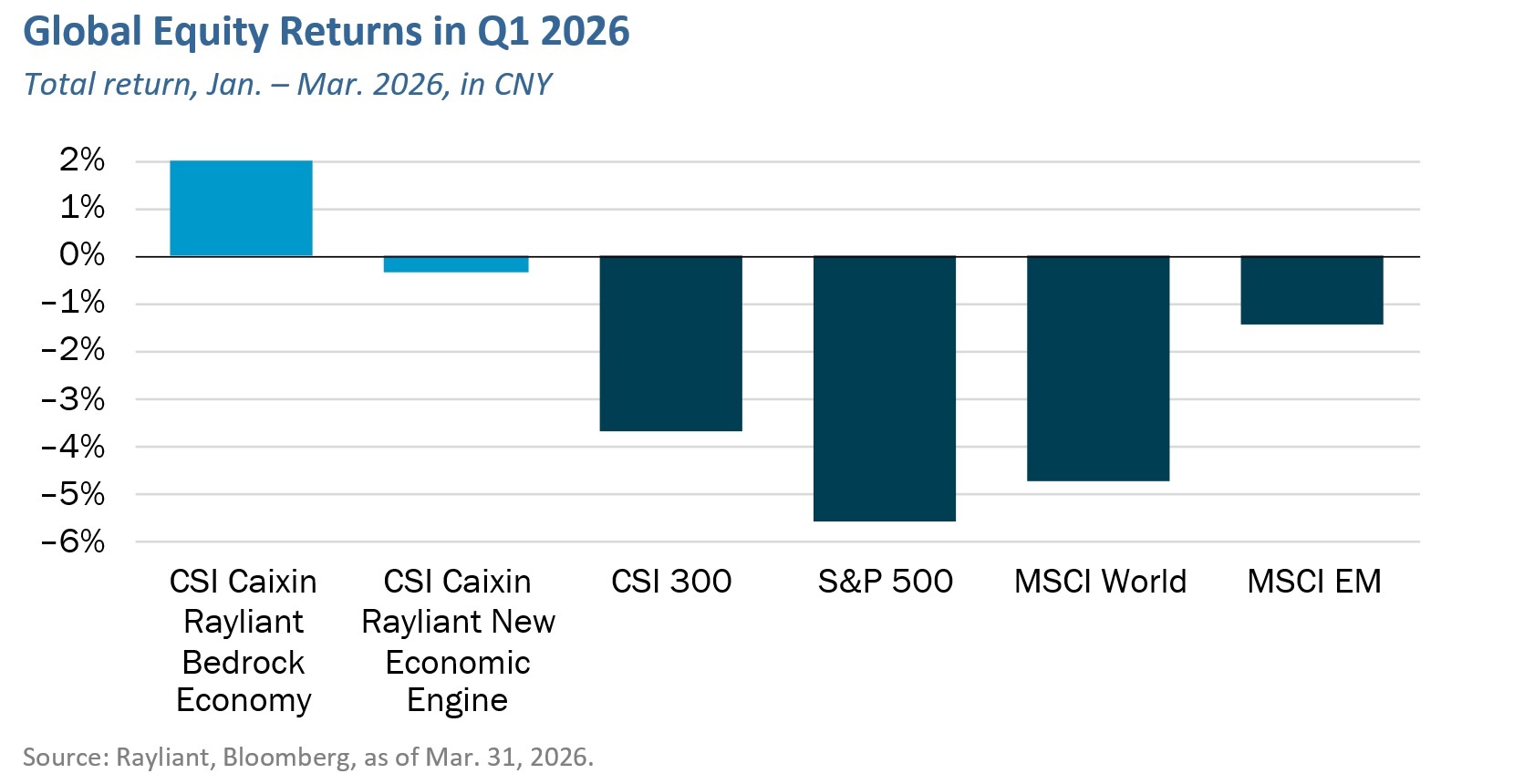

Despite getting off to a decent start in 2026, Chinese stocks sold off as conflict erupted in the Middle East, with the CSI 300 Index finishing the quarter down 3.7% (CNY) over the three months ending December 31st, 2025, as shown below. That was still better than the return on US stocks in Q1, as the S&P 500 posted a 5.6% (CNY) decline, made worse by a sell-off in software names—the S&P Software Industry Index ended the quarter nearly 25% lower in CNY terms—as fears over AI disruption reached the “SaaSpocalypse” level, driving a wedge between IT hardware and services shares. Emerging markets fared considerably better, falling by just 1.4% (CNY); indeed, it was tech-heavy markets like Taiwan and Korea, rallying on the back of large exposures to hardware stocks in the “AI winner” category, that provided EM more cushion to absorb March’s war-induced drawdown. International developed stocks in the MSCI World Index modestly outperformed the US in Q1.

Against a fraught geopolitical backdrop in the first quarter, both the Bedrock and New Economy strategies provided shelter from the storm, with the CSI Caixin Rayliant Bedrock Economy Index (tracked by Premia’s 2803 HK/9803 HK ETFs) actually gaining 2.0% (CNY), and the CSI Caixin Rayliant New Economic Engine Index (tracked by Premia’s 3173 HK/9173 HK ETFs) notching only a modest decline of 0.3% (CNY) in the first three months of the year. At the factor level, the Bedrock strategy clearly enjoyed an edge from its decisive tilts toward Value and Low Risk stocks, while Growth underperformance weighed on the New Economy portfolio, offset by small-cap exposure, which turned out to benefit both strategies in Q1. From a sector standpoint, the Bedrock strategy saw strong contribution from an overweight to Energy stocks—which led sectors within the CSI 300 as oil prices spiked on the Middle East conflict—along with strong selection among Financials and Utility names. An underweight to Energy stocks, by contrast, was the biggest detractor within the New Economy portfolio, though that was more than made up for by effective stock-picking within IT shares and Industrials, as well as a timely underweight to Financials, which faced a relatively large drawdown in Q1.

Going forward, we view China’s onshore stock market as especially well-positioned among Emerging Markets to persevere through times of increased geopolitical stress, and believe the AI “fear trade”, which has hampered some technology investments, is somewhat overdone. In fact, as results of the ETFs in Q1 demonstrate, short-run macro volatility and fears of disruptive technological change can actually be a spur for mispricings: the very behavioral mistakes that the Bedrock and New Economy strategies’ factor exposures are built to uncover and exploit. Such dynamics make turbulence in Chinese equities a potential opportunity to establish positions in the portfolios that we expect to pay off when fundamentals eventually take over from investors’ greed and—more relevant in today’s environment—fear in driving longer-term returns.

*****************************************************************************************************

Dr. Phillip Wool is the Global Head of Research of Rayliant Global Advisors. Phillip conducts research in support of Rayliant’s products, with a focus on quantitative approaches to asset allocation and return predictability within asset classes, as well as the design of equity strategies tailored to emerging markets, including Chinese A shares. Prior to joining Rayliant, Phillip was an assistant professor of Finance at the State University of New York in Buffalo, where he pursued research on quantitative trading strategies and investor behaviour, and taught investment management. Before that, he worked as a research analyst covering alternative investments for Hammond Associates, an institutional fund consultant. Phillip received a BA in economics and a BSBA in finance and accounting from Washington University in St. Louis, and earned his Ph.D. in finance from UCLA, where his research focused on the portfolio holdings and trading activity of mutual fund managers and activist investors. Premia CSI Caixin China New Economy ETF and Premia CSI Caixin China Bedrock Economy ETF track the CSI Caixin Rayliant New Economic Engine Index and CSI Caixin Rayliant Bedrock Economy Index respectively.