Efforts going back over a decade have already paid off in world-class, non-linear progress in applications and design. China’s AI “arrival” prompted Nvidia’s Jensen Huang to warn that it was only "nanoseconds behind," the US. In chip design, China's fabless industry has seen a stunning six-fold increase in its number of companies since 2010. Certain products from leading Chinese chipmakers such as Huawei, Cambricon and Hygon are catching up with the performance of some of Nvidia’s and AMD’s chips.

In logic foundry, SMIC’s 7nm process—famously used for Huawei's Kirin processors—is reportedly finalizing a 5nm-equivalent process. In memory foundry, China’s YMTC and CXMT are narrowing the capability gap against South Korea’s Samsung and SK Hynix. And there have been many other achievements and breakthroughs.

But China is still fundamentally constrained by a critical, decade-wide gap in manufacturing equipment. To bridge that gap, China has responded with a high-cost, high-stakes national strategy: to leverage its strengths in AI and design and its huge domestic market to justify and fund an independent workaround for this core manufacturing bottleneck.

This report explores China's current standing in the global chip race and how this asymmetric battle for tech sovereignty will impact the investment landscape in the near future. This is a fight in which hundreds of billions of Dollars will be invested in building China’s capabilities – something already clearly preferred over the softer option of accepting older generation chips offered by the US. This will be a battle which will see accelerated import substitution offering opportunities to Chinese tech companies.

Uniquely positioned within this landscape, the Premia China New Economy ETF (3173/9173 HK) and Premia China STAR50 ETF (3151/9151 HK) are calibrated to capture the beta of domestic key beneficiaries and the alpha of long-term value emerging from this secular trend of self-sufficiency and domestic substitution. Concurrently, the Premia Asia Innovative Technology & Metaverse ETF (3181/9181 HK) is strategically positioned to deliver regionally diversified access to the surging investment and rapid technological adoption fuelled by AI acceleration across the wider Asian region.

The thriving "brain": strengths in AI, applications, and design

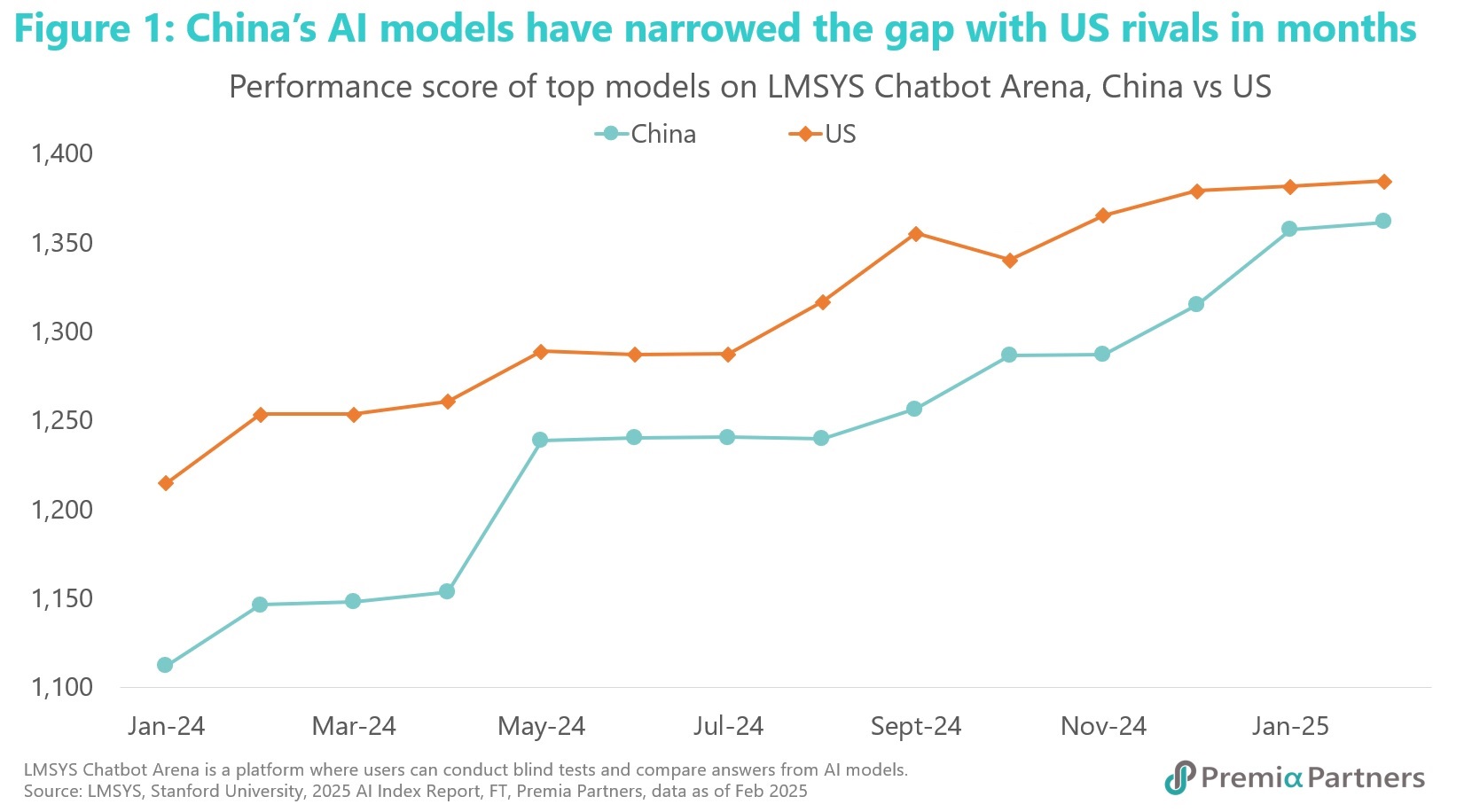

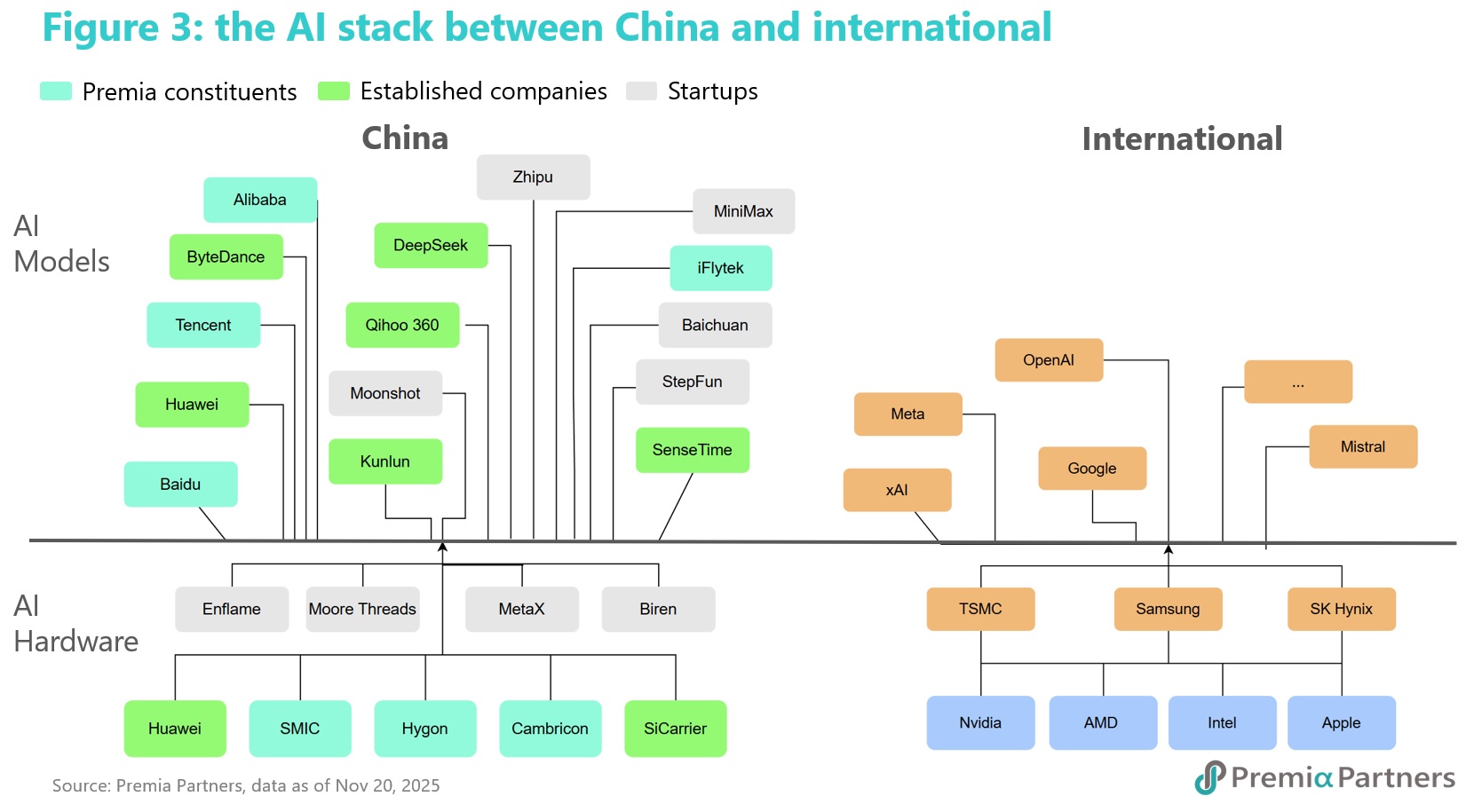

China's most potent asset in the chip war is its massive, dynamic domestic market and its rapidly advancing "brain" in software and design. In Generative AI, China is not lagging, it is competitive. The country's AI user base had exploded to over 515 million1 as of mid-2025, creating a fertile ground for innovation and adoption. Domestic models from firms such as DeepSeek, Alibaba (Qwen), Baidu (Ernie), ByteDance (Doubao), Moonshot (Kimi), and Zhipu AI (GLM) are closing the performance gap with Western counterparts like OpenAI (ChatGPT) and Google (Gemini). Nvidia CEO Jensen Huang repeatedly warned that this gap is now only "nanoseconds behind”2 US AI. So Chinese AI has shortened a gap of years to seconds in just a few months. In the open-source sphere, these Chinese models are dominant, frequently topping global leaderboards and seeing adoption even by US and EU startups.

In chip design—the silicon "brain"—China's fabless industry is robust, boasting over 3,600 companies as of late 2024, a sixfold increase since 20103. This strength means that as soon as new manufacturing capabilities come online, domestic designers are ready to flood the market with advanced blueprints. Huawei's HiSilicon, for example, has long designed world-class, 5nm-level "Kirin" processors, proving China has the intellectual horsepower to design cutting-edge logic.

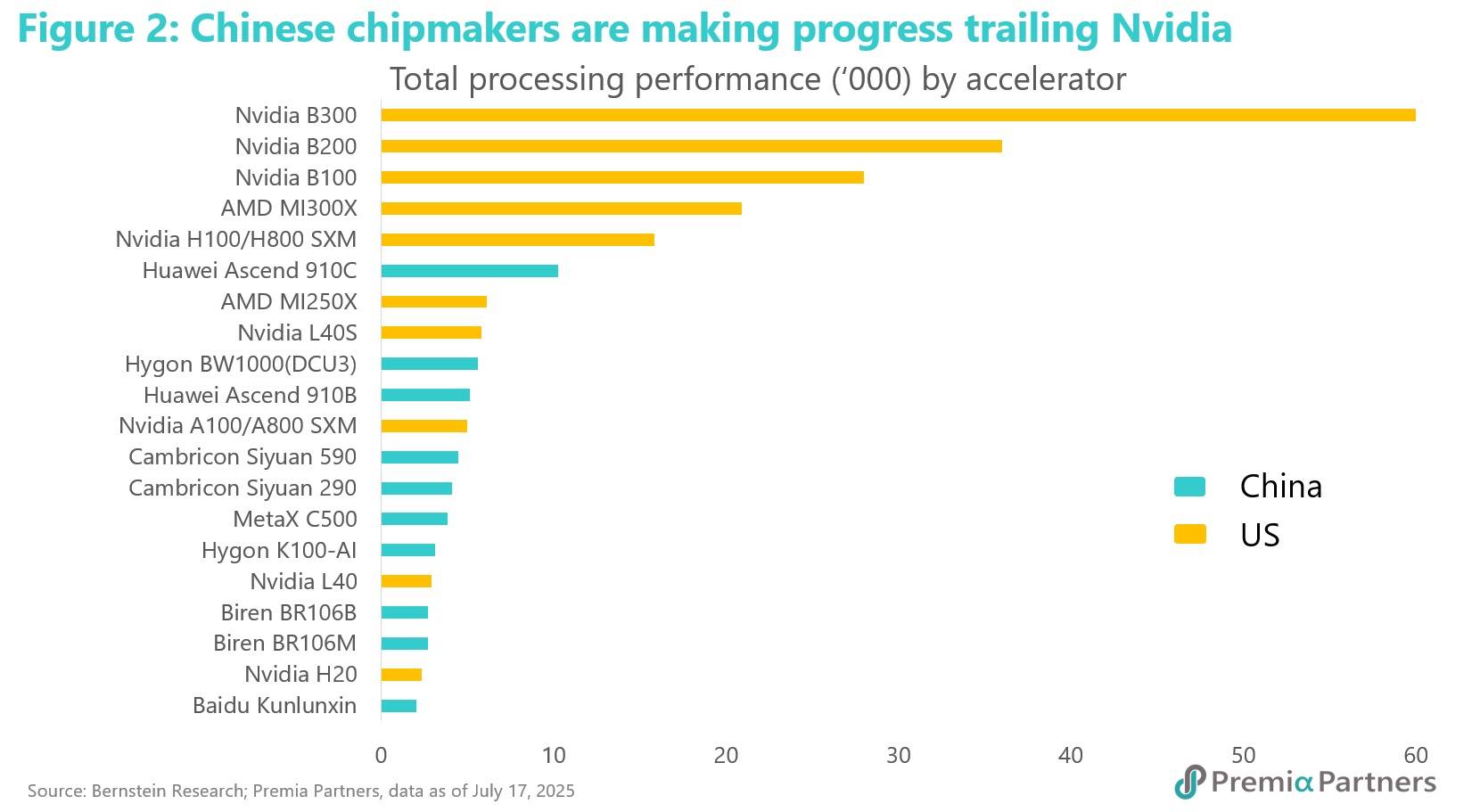

While Nvidia’s CUDA and AMD’s ROCm are still top ranked in performance and preferred by the global majority, leading Chinese chipmakers such as Huawei, Cambricon and Hygon are aggressively eroding this moat. Huawei’s new Ascend 910B chip is widely considered on par with or slightly better than Nvidia’s A1004. According to TrendForce5, the 910C can deliver 60-70% of the performance of Nvidia’s H100, with the upcoming 910D expected to surpass it. Cambricon, often called "China’s little Nvidia," has a product line evolving rapidly; its current Siyuan 590 achieves about 80%6 of Nvidia’s A100 performance, and the follow-up Siyuan 690 is positioned to rival the H100.

Perhaps traditionally recognized for its x86-architecture central processing units, which bear similarities to AMD’s designs, Hygon has successfully reoriented its core focus towards the accelerator space. This shift is headlined by its DCU-branded General-Purpose GPU (GPGPU)-like components, which crucially operate within a CUDA-compatible ecosystem. Its flagship product, the DCU3 (BW1000), is positioned as one of the most highly competitive offerings in the local territory and is projected to become a significant contributor to the company’s revenue stream this fiscal year.

Meanwhile, Baidu’s Kunlunxin and the “Four Little Dragons”—Enflame, Moore Threads, MetaX, and Biren—constitute another competitive cohort of domestic GPU solution providers. These entities, while presently trailing Nvidia in overall product performance and maturity, have nonetheless elevated the pursuit of full compatibility with Nvidia’s proprietary CUDA platform to a top-level strategic priority: to minimize developer migration costs in both software and hardware, and critically, to seamlessly facilitate client adoption. This accelerating software capability represents a far greater long-term competitive threat to the CUDA hegemony than hardware parity alone. Adding to this strategic momentum is the notable IPO of Moore Threads, which launched on the STAR Market to raise approximately RMB 8 billion, marking the largest fundraising round on the board last year7. This substantial capital infusion is specifically earmarked to aggressively advance the R&D of its self-developed MUSA architecture, funding the next generation of integrated AI training/inference chips, graphics processors, and AI System-on-Chip (AISoC) projects.

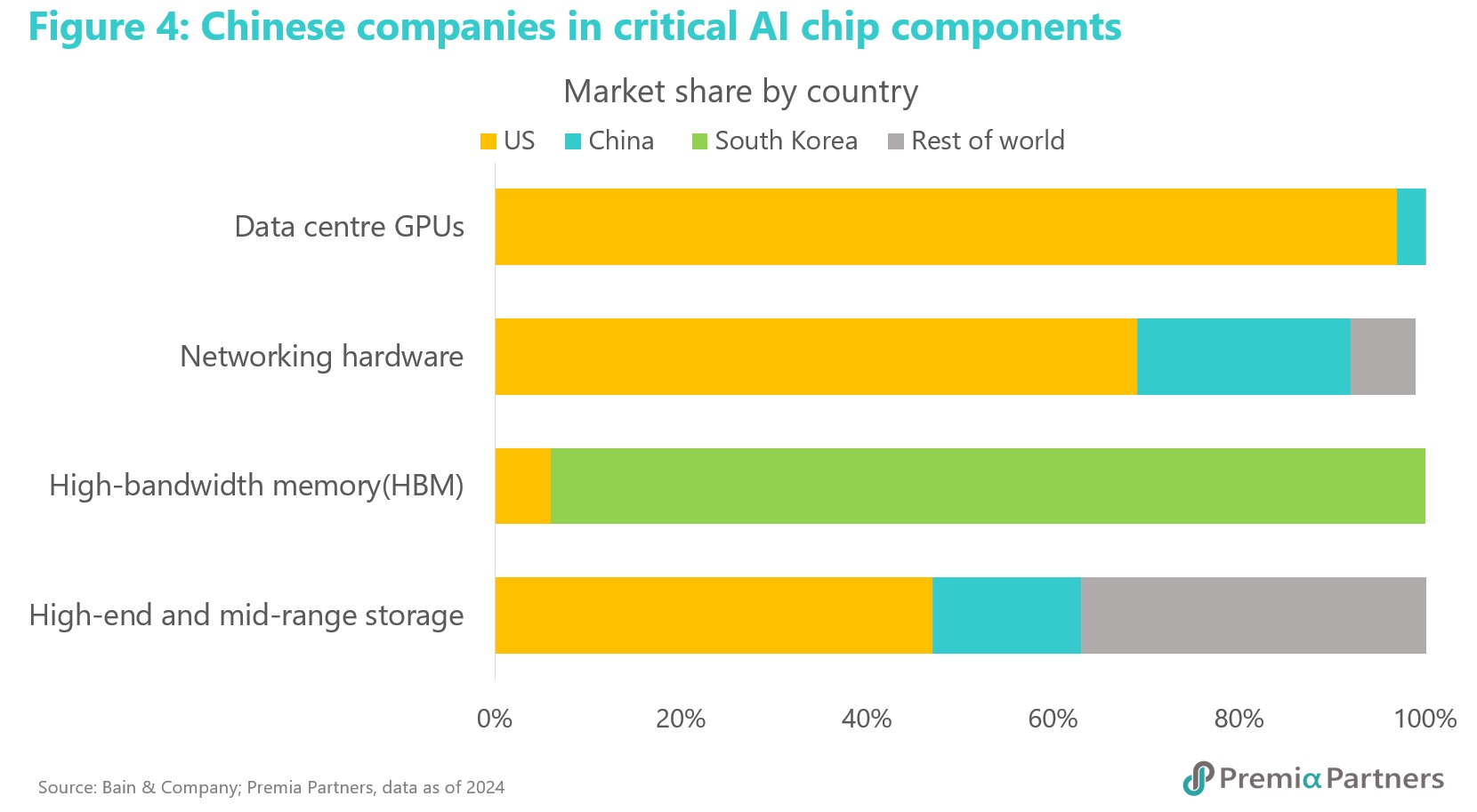

However, this "brain" has a critical vulnerability in its "nervous system": Electronic Design Automation (EDA) software. China remains dependent on foreign software to design its most advanced chips, with the market 74%8 dominated by US firms like Synopsys, Cadence, and Siemens. Yet domestic players such as Huawei-linked SiCarrier's subsidiary, Qiyunfang, are emerging—claiming a 30%8 design efficiency increase and shortening hardware development cycles by 40% compared to US tools. The challenge now is finding a domestic foundry capable of building what these tools design.

The hardened "Engine": fuelling the dual race in legacy and advanced fabrication

In logic foundry, China's strategy involves a two-pronged approach: pushing the limits of advanced logic using older equipment and dominating the global market for mature, specialized chips. SMIC, China's answer to TSMC and the largest domestic chipmaker, ranks as the 3rd largest9 foundry globally by revenue in 2024. At the cutting edge, SMIC’s 7nm process—famously used for Huawei's Kirin processors—is reportedly finalizing a 5nm-equivalent process. However, because SMIC lacks EUV machines, this production relies on older Deep Ultraviolet (DUV) lithography and complex, costly techniques such as Self-Aligned Quadruple Patterning (SAQP), according to Tom’s Hardware analysis10.

Hua Hong Semiconductor, China's second-largest foundry, operates in a different sphere. As a specialist, it does not compete at the 7nm/5nm cutting edge; its most advanced nodes are 28nm/22nm. Hua Hong's strength lies in specialized processes like embedded non-volatile memory (eNVM) and power discrete devices, which are critical for electric vehicles and industrial machinery. This focus on "legacy" but vital chips insulate it from the direct impact of advanced-node sanctions and allows it to capture massive government-backed domestic demand.

In memory foundry, although South Korea’s dominance persists in the global market, China's champions are demonstrating immense influence domestically this year. YMTC (Yangtze Memory Technologies Corp) is China's top NAND flash maker, while CXMT (ChangXin Memory Technologies) is a major success story in DRAM. In NAND flash, YMTC began mass-producing 270-layer 3D NAND chips earlier this year, successfully narrowing the technology gap with SK Hynix’s 321 layers and Samsung’s 286 layers11. The company is expected to leapfrog to 400-layer NAND in the second half of this year, skipping the 300-layer milestone. In the DRAM sector, CXMT is shaking up the market by selling previous-generation DDR4 chips at roughly half the price of competitors, leading industry observers to predict that the current three-way dominance by Samsung, SK Hynix, and Micron may soon collapse. This competitive threat became even more tangible following a DigiTimes report12 stating that YMTC is strategically partnering with CXMT to explore the development of High Bandwidth Memory (HBM)—the premium DRAM required for flagship AI accelerators and High-Performance Computing (HPC)—as a concerted effort to support the domestic market in the face of western dominance.

The "Muscle": a manufacturing bottleneck

The primary, acute shortage for China is the "muscle" to build its advanced designs: manufacturing equipment. Successive rounds of US sanctions blocked the export of ASML’s Extreme Ultraviolet (EUV) systems and even advanced models of Deep Ultraviolet (DUV) systems. China is dependent on foreign tools: 33% of ASML’s 2025 sales13 were DUV systems shipped to China, however, the share is expected to decline to ~20% in 2026. To counter this, a state-backed ecosystem led by firms like SiCarrier is being built to create a full-stack domestic alternative, covering everything from etching (EPI, CVD, PVD) to materials like photoresists (via its subsidiary Skyverse).

But the core lithography tool remains elusive. The most advanced domestic tool currently being tested by SMIC is from Yuliangsheng (a subsidiary of SiCarrier), a 28nm-class DUV machine. Technical analysis by Tom’s Hardware14 suggests this system is comparable to an ASML Twinscan NXT:1950i model from 2008—generations behind ASML’s popular NXT:2000i for 7nm and 5nm class nodes. While this represents a crucial step toward self-sufficiency, it simultaneously substantiates the claims made by ASML’s CEO regarding a 10-to-15-year technology gap.

The technological workarounds: “bypass” strategies in the EUV race

To bridge the gap between its advanced design needs (driven by AI) and its lagging equipment reality, China has resorted to a costly workaround: using older DUV tools with advanced Self-Aligned Quadruple Patterning (SAQP). This is how SMIC reportedly produces its 7nm-class Kirin 9000S chip for Huawei10. This strategy is commercially unviable by Western standards but vital for China's national security. Institutional data suggests SMIC's 5nm-class wafers produced this way could cost up to 40-50%15 more than TSMC's EUV-based equivalents, and 7nm yields are reportedly in the 60-70% range16, far below the industry standard. Despite cost and yield compromises, China is engaged in non-linear catch-up in the DUV race by paying a "sanction tax."

Beyond SiCarrier, another firm, AMIES Technology—a spin-off of Shanghai Micro Electronics Equipment (SMEE)—drew attention for its advances in lithography at the recent SemiBay 2025 event. They showcased a diverse portfolio including compound semiconductor lithography machines, laser annealing systems, and solutions for packaging and wafer bonding. The company reportedly holds 35%17 of the global market for advanced packaging lithography and around 90% of the domestic market. Although its core technology is used for 90nm and above production and does not challenge ASML’s EUV dominance yet, it fills critical domestic gaps and supports China’s growing need for AI, EV, and industrial chips.

More speculative, high-risk bets include Nanoimprint Lithography (NIL) tools; China's Prinano Technology delivered a domestic tool with sub-10nm capabilities in August18. Even though the technology is not yet applicable for logic chips like CPUs or GPUs, the pursuit of a potential non-ASML path to EUV is always part of the equation for Chinese companies.

So, where is China now in the chip race?

Simply put, China is not yet at the cutting edge of the chip industry. But China's position is that of an asymmetric power: a world-class leader in applications (AI) and design (fabless), and quite competitive in foundry, despite being weak in the foundational layer of manufacturing equipment. But to address this critical gap in semiconductor manufacturing equipment, China is willing to pay the price to avert hurdles to achieve technology independence. By leveraging its market and design strengths to fund a long, innovative war of technological attrition, China is signalling it will trade efficiency for independence at this stage of its development.

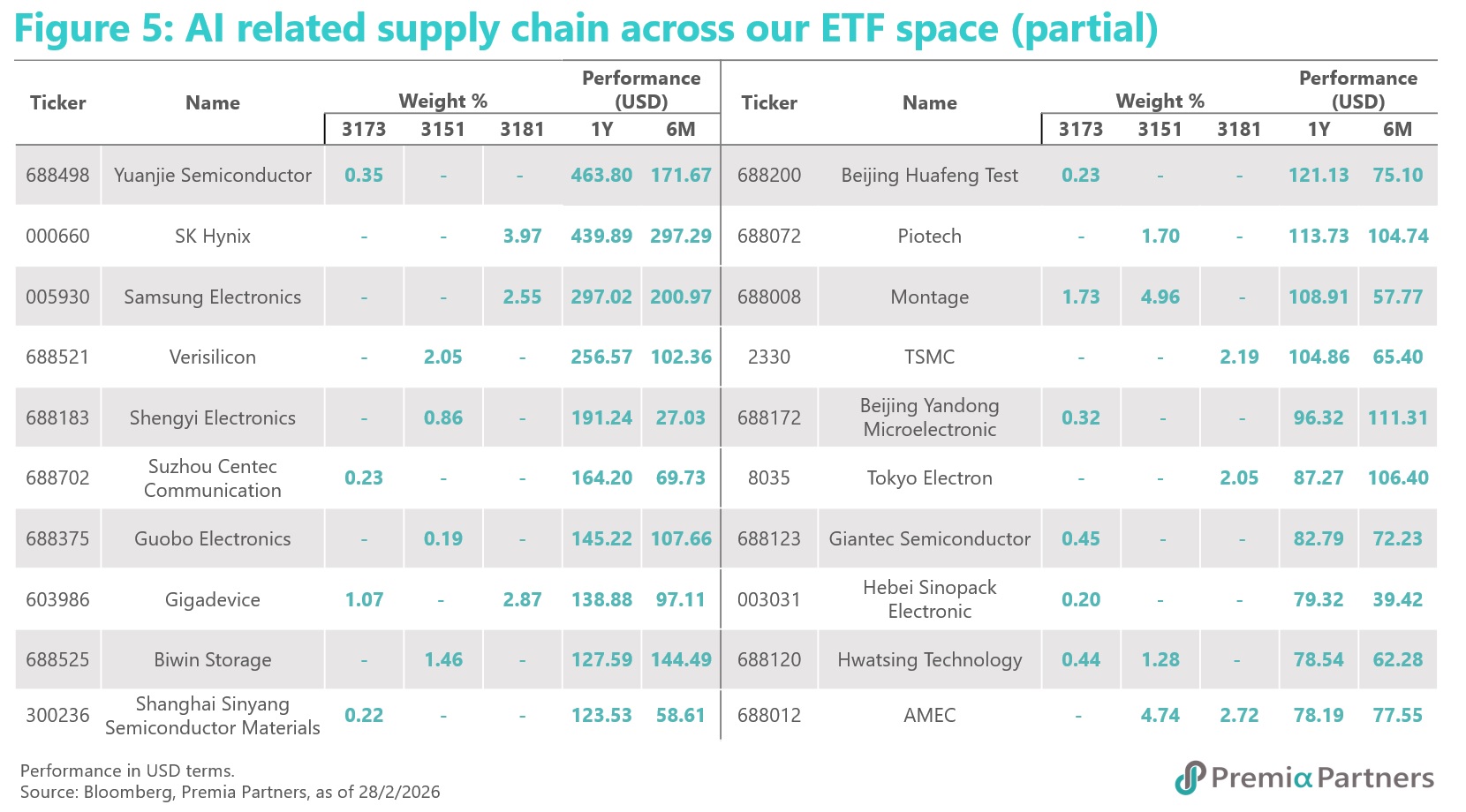

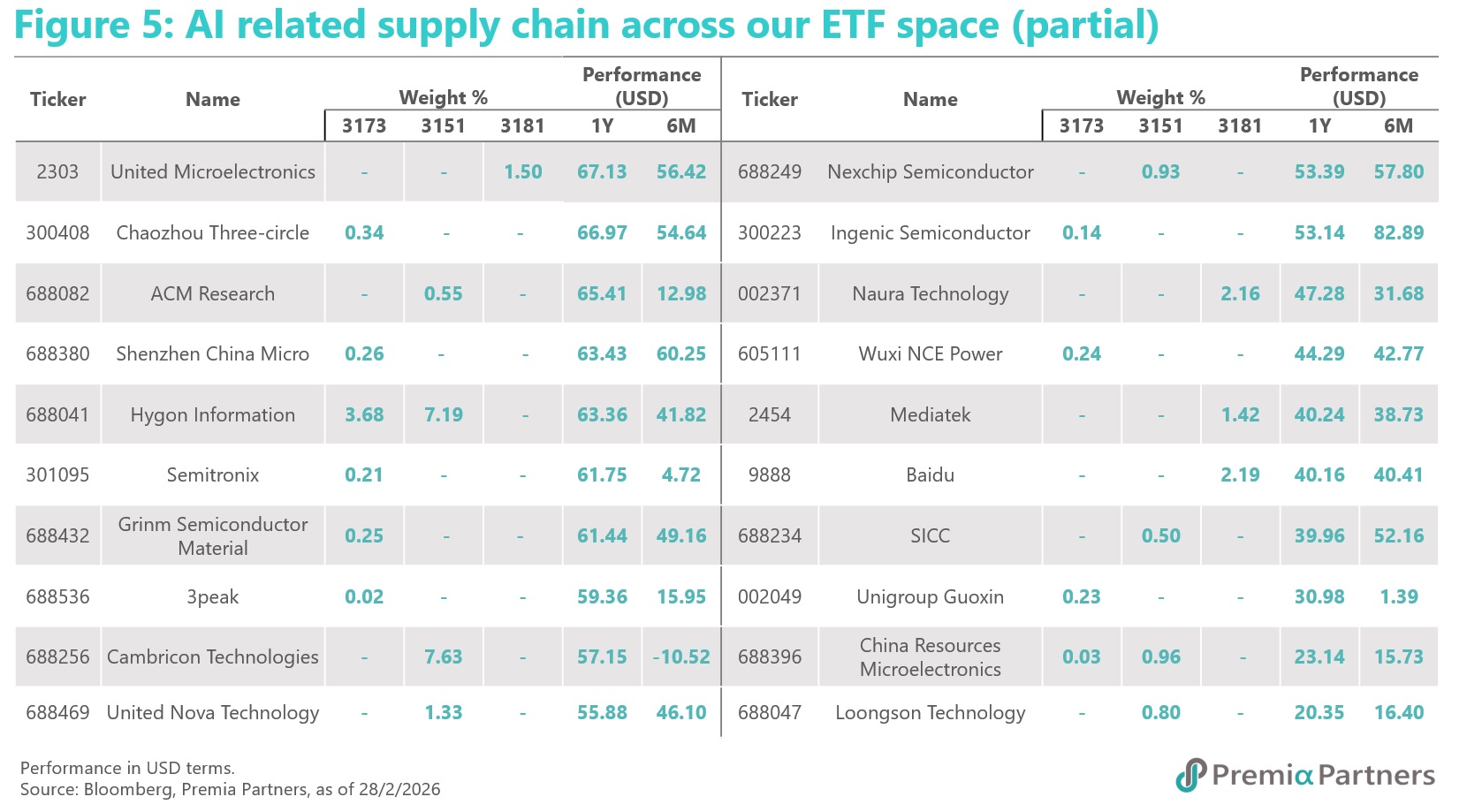

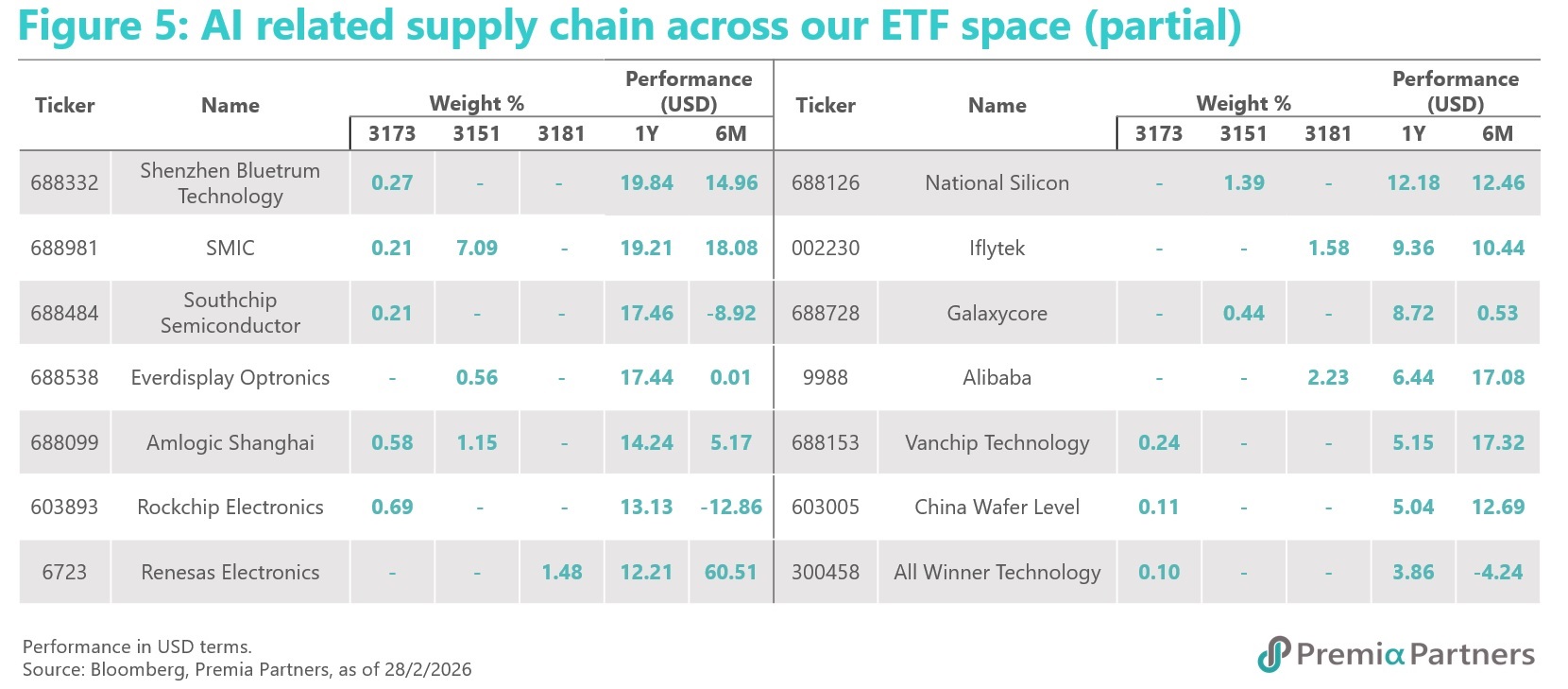

As the domestic substitution trend accelerates, a distinct set of winners is emerging across China’s entire technology stack. This drive for sovereignty is unlocking immense value, not just for foundries like SMIC, but also for the critical equipment manufacturers filling the void left by foreign export restrictions, including market leaders like Naura Technology and AMEC. This momentum extends seamlessly to AI chip pioneers such as Cambricon and Hygon, and further to downstream application giants like Kingsoft Office and the dominant cloud providers, Alibaba, Tencent, and Baidu, which are actively commercializing this new domestic infrastructure.

Uniquely positioned to capture the financial opportunity stemming from this secular trend, the Premia China New Economy ETF (3173/9173 HK) and Premia China STAR50 ETF (3151/9151 HK) are calibrated to capture the domestic exposure of these key beneficiaries alongside the excess return generated by long-term industry value creation across vital sectors including AI-driven hard-tech, Electric Vehicles (EVs), batteries, and biotech. Meanwhile, the Premia Asia Innovative Technology & Metaverse ETF (3181/9181 HK) serves as a regionally diversified avenue to capture the escalating demand and investment surrounding AI acceleration across the broader Asian region, encompassing major markets such as Japan, South Korea, Taiwan, and Singapore, in addition to China. All three ETFs have validated this investment thesis by delivering impressive USD NAV returns over the past year of approximately 28%, 39% and 40% respectively as of 28 February 2026.

Source

- SCMP, China’s generative AI user base doubles to 515 million in 6 months, Oct 20, 2025

- SCMP, China is ‘nanoseconds behind’ US in chips, Nvidia’s Jensen Huang says, Sep 28, 2025

- CSIS, Innovation Lightbulb: Innovation Competition in Chip Design Between the U.S. and China, Feb 21, 2025

- SCMP, Huawei says its AI chip better than Nvidia’s A100 amid China’s self-reliance drive, Jun 6, 2024

- TrendForce, Decoding Huawei’s DeepSeek All-in-One Machine: 60-70% of NVIDIA H100 Performance at an Appealing Price, Apr 29, 2025

- TrendForce, Is Cambricon the Next NVIDIA or Unsustainable Growth Story? Three Key Risks Behind the Epic Rally, Aug 27, 2025

- ANUE, China-U.S. Computing Power Competition Escalates! Domestic Chip Giants HiSilicon and Sugon Merge Experts: China's Version of “NVIDIA-AMD” Has Emerged, May 28, 2025

- TrendForce, China’s largest STAR Market IPO of 2025, Moore Threads, Goes Public on Nov 24, Raising RMB 8B, Nov 24, 2025

- TrendForce, SiCarrier Subsidiaries Reportedly Launch China’s Fully Independent EDA, 3nm Test Equipment, Oct 15, 2025

- The Motley Fool, Ranked: Semiconductor manufacturers by global revenue, Sep 5, 2025

- Tom’s Hardware, Huawei patent reveals 3nm-class process technology plans — China continues to move forward despite US sanctions, May 29, 2024

- TrendForce, China’s YMTC Launches $3B Wuhan Phase III Venture, Signaling NAND Expansion Ambitions, Sep 9, 2025

- DigiTimes, China's YMTC moves into DRAM, teams with CXMT to target HBM market, Sep 2, 2025

- Reuters, ASML plays down Chinese tool stockpiling, impact of rare earth restrictions, Oct 15, 2025

- Tom’s Hardware, China's largest chipmaker testing first homegrown immersion DUV litho tool — SMIC takes significant step on road to wafer fab equipment self-sufficiency, Sep 17, 2025

- TechPowerUp, SMIC Reportedly On Track to Finalize 5 nm Process in 2025, Projected to Cost 40-50% More Than TSMC Equivalent, Mar 29, 2025

- Anysilicon, Global Foundry Earnings Q3 2025: Growth Diverges as AI, Specialty Nodes and 2nm Ramps Reshape the Market, Nov 18, 2025

- SCMP, Meet AMIES, China’s new hope in breaking reliance on ASML’s chipmaking machines, Oct 19, 2025

- Bits&Chips, China’s Prinano delivers first domestic nanoimprint litho tool, Aug 19, 2025