The geopolitical shockwaves from the Iran conflict have triggered a sharp repricing across global asset markets, with crude oil surging, gold retreating, Treasuries selling off, and cracks beginning to appear in US technology equities, arguably the most crowded trade among global institutional portfolios. Against this backdrop of elevated geopolitical risk, Federal Reserve policy uncertainty, and stretched valuations in the US, the case for meaningful diversification has rarely been more persuasive. We believe China tech represents not merely a tactical hedge, but a structurally grounded, high-conviction opportunity that could well be the next generation source of alpha for discerning investors.

The strategic signal from China’s most recent “Two Sessions” could not be clearer: innovation and technological self-reliance have been elevated from economic objectives to core pillars of national strategy. The government is directing resources toward breakthrough technologies, including semiconductors, artificial intelligence, quantumand aerospace technologies, and advanced manufacturing, with a sense of urgency sharpened by ongoing geopolitical tensions. Indeed, the policy framework has evolved beyond fragmented support measures. Beijing is building an integrated innovation system that connects basic research, applied R&D, industrial production, capital, and talent, backed by rising science funding and closer coordination between the state, universities, and the private sector.

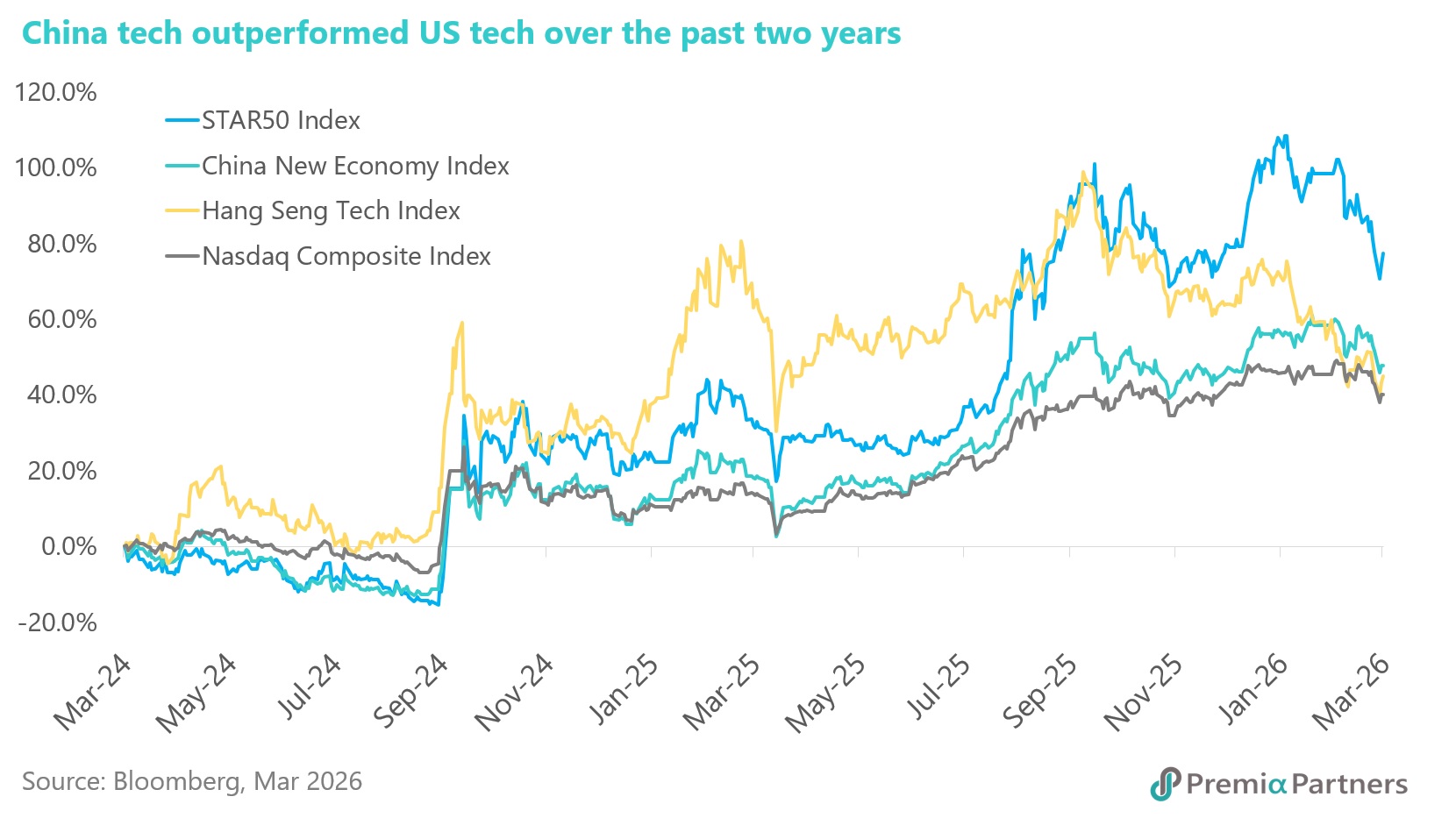

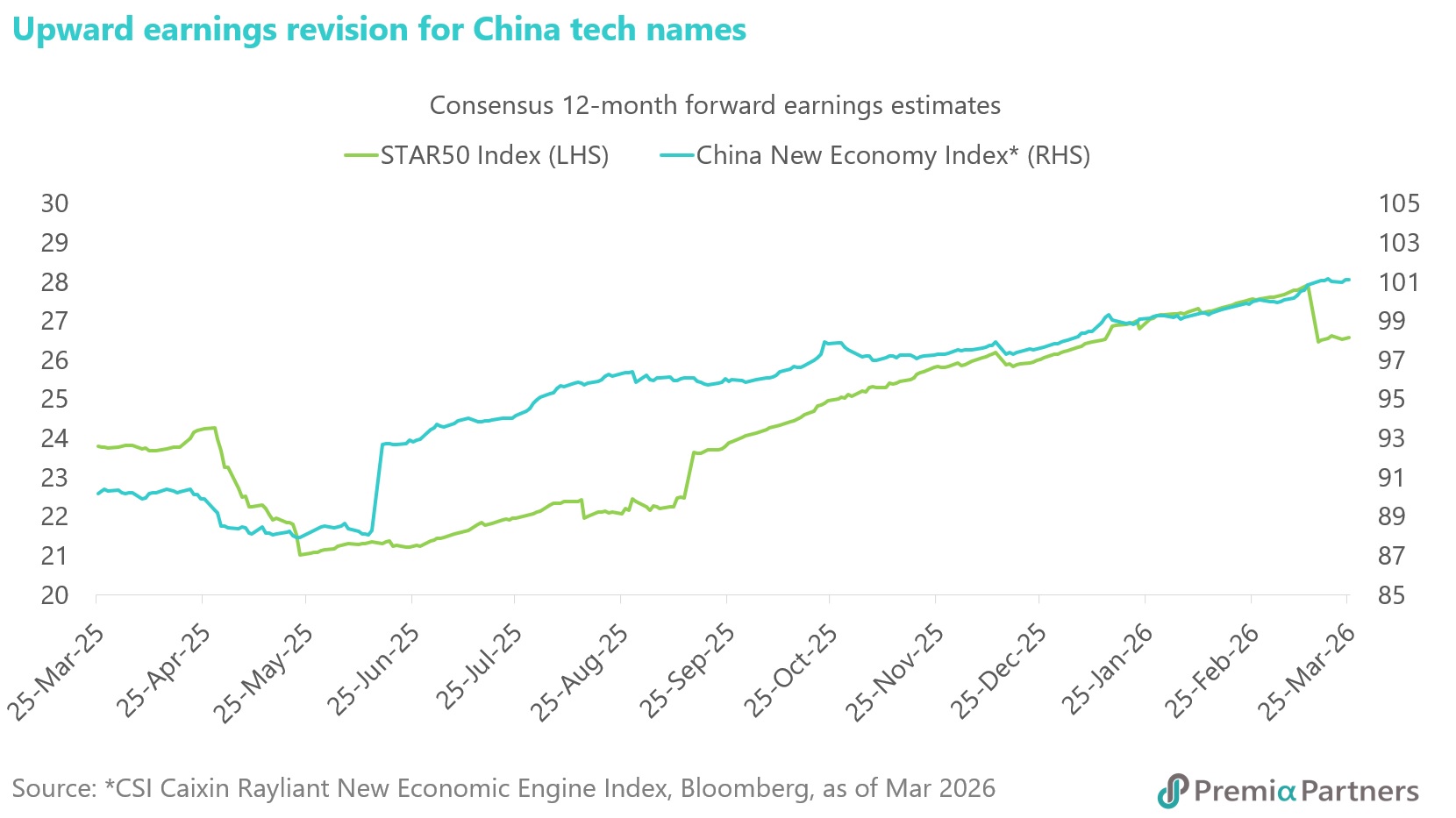

A common misconception among investors is that China tech has been a poor performer, but the data tells a very different story. Over the past two years, China tech has delivered returns that comfortably surpassed those of its US counterparts. The STAR50 Index, which concentrates on China’s leading hardcore technology companies, generated a total return of 77.3%. The China New Economy Index and the offshore Hang Seng Tech Index both returned in excess of 45%, versus a 40.2% gain for the Nasdaq over the same period.

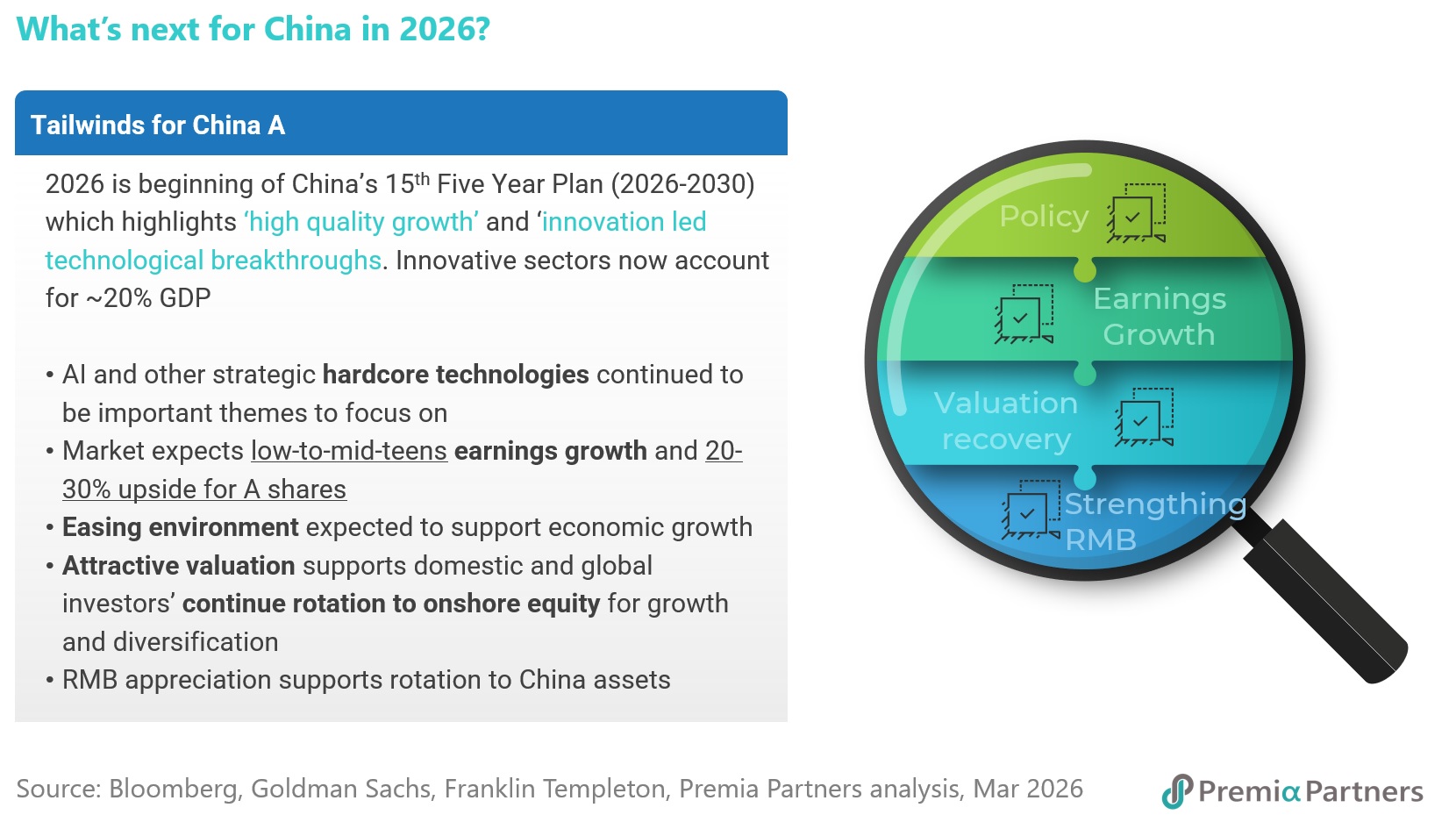

2026 marks the start of China's 15th Five-Year Plan, making it a pivotal year for the investment thesis. Innovation is now the central pillar of China's long-term growth plan, captured under the government's 'new quality productive forces' framework. This represents a deliberate departure from the old playbook of property-led investment and infrastructure stimulus, and a contrast to Western economies reliant on loose credit and overconsumption. Instead, China is moving purposefully toward AI-enabled productivity gains, high-tech manufacturing, new energy, and advanced materials. Policy emphasis is equally placed on cultivating deep talent pipelines, promoting open-source AI ecosystems, and guarding against wasteful competition and overcapacity, reflecting a maturing and disciplined approach to growth strategy.

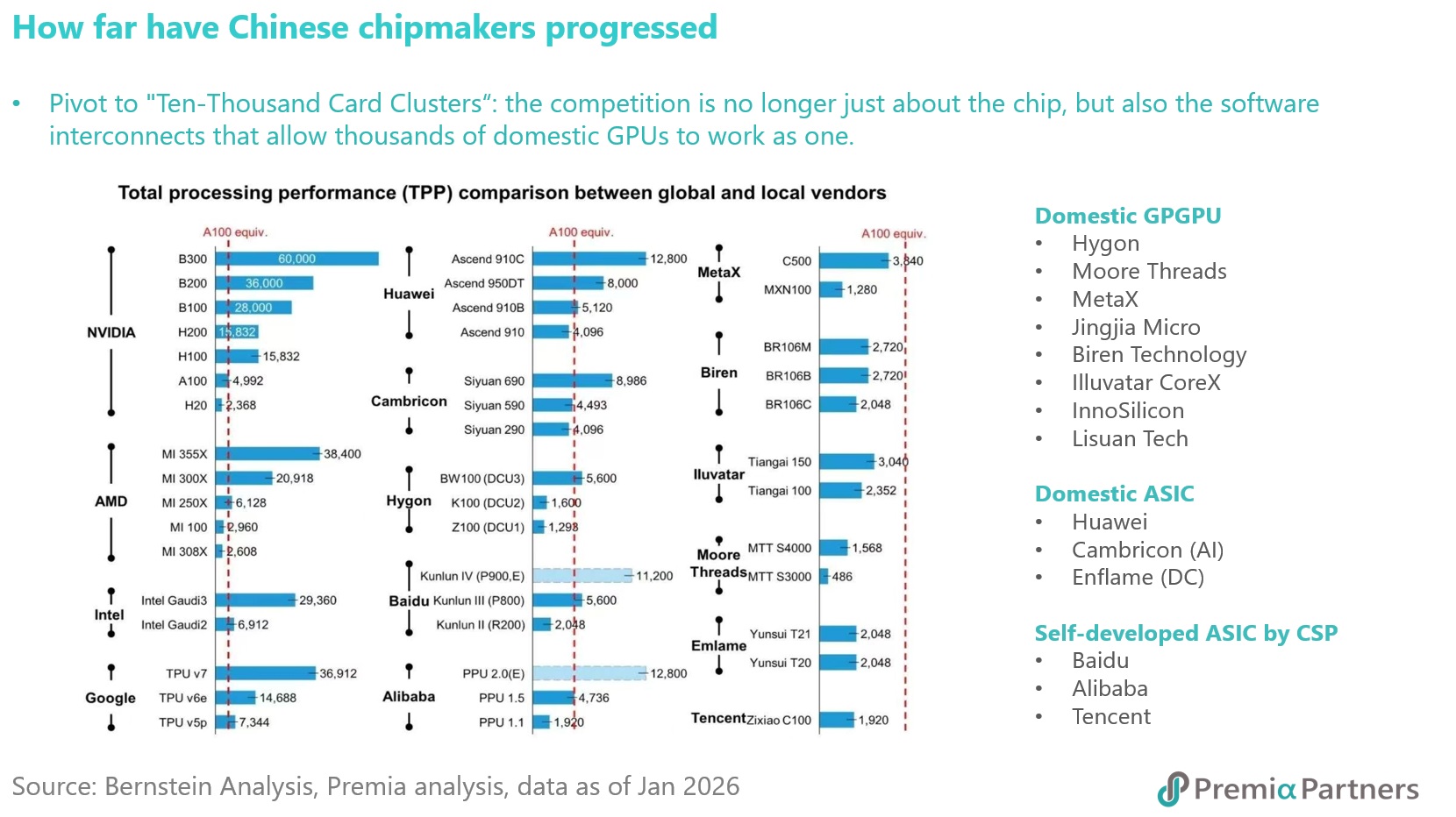

On the technology front, China is making tangible progress in building its own capabilities. In semiconductors, while Chinese firms have not yet matched the raw processing performance of leading single chips from Nvidia or AMD, they have engineered a practical alternative. Facing export restrictions that limit access to the most advanced GPUs, Chinese companies have pivoted to large-scale horizontal clustering. Rather than relying on fewer, cutting-edge chips, they deploy thousands of mid-tier or domestically produced GPUs networked to function as a unified supercomputer. These 'Ten-Thousand Card Clusters', which aggregate 10,000 or more GPU accelerators, are already being used to train frontier AI models at scale. In effect, China is redefining the terms of the technology race, shifting the competition from 'best chip' to 'best computing system' by leveraging scale, systems architecture, and deep software integration to offset hardware constraints.

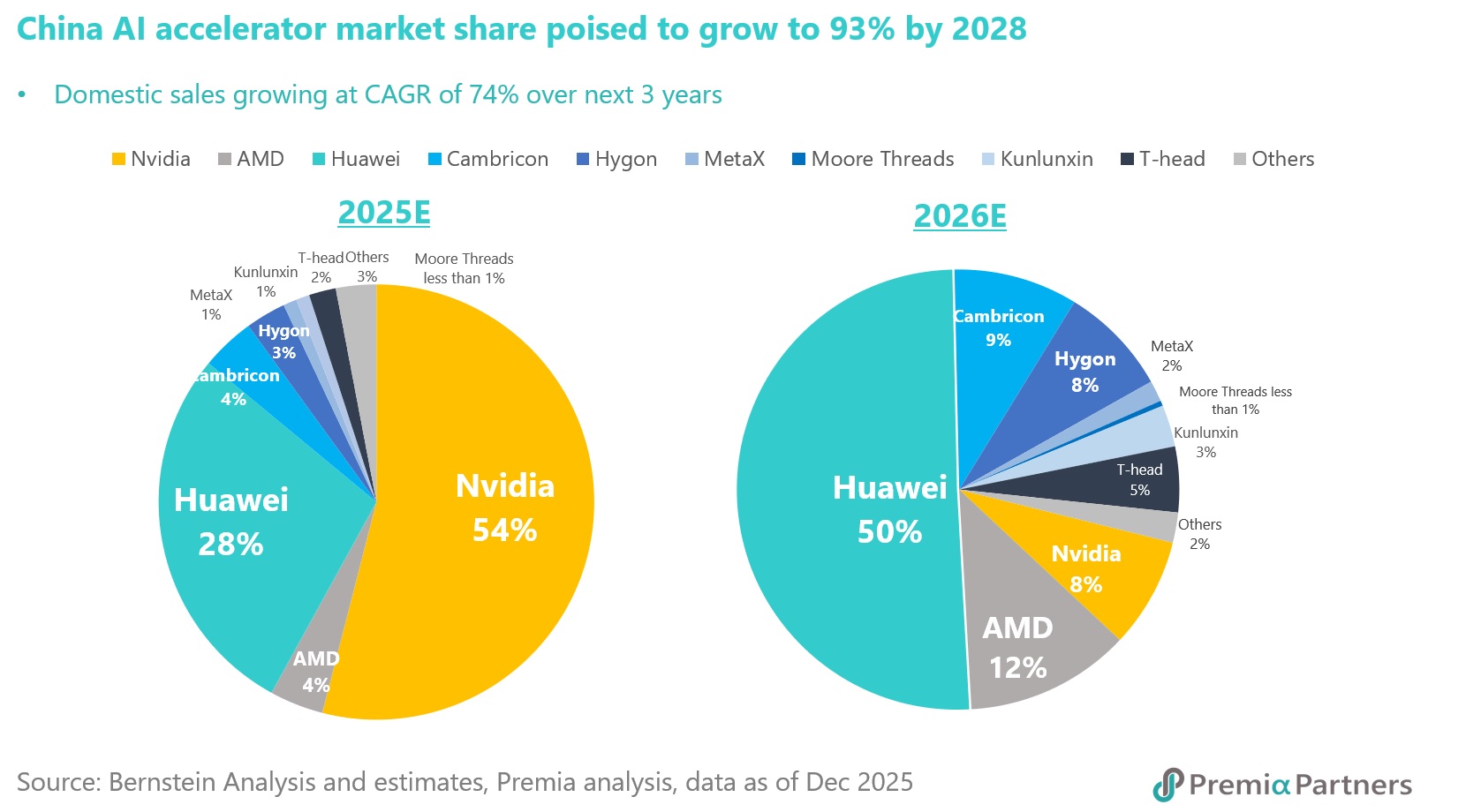

The momentum behind domestic substitution is powerful and increasingly irreversible. The AI accelerator market in China illustrates this dynamic with striking clarity. As recently as 2025, Nvidia and AMD commanded approximately 60% of the market. That landscape has fundamentally shifted. Driven by both regulatory push factors in the US and strategic pull factors in China, domestic suppliers are on track to capture close to 80% of the market this year, leaving foreign vendors with a rump 20% share. Critically, even if technology transfer restrictions were to be lifted tomorrow, the path back for foreign companies would be steep, as Chinese clients have already re-engineered their workflows around domestic chips, integrating them into their technology stacks, pricing models, and supply chain operations. The lesson drawn from the Iran conflict, that strategic technology dependence on foreign sources carries unacceptable national risk, will only accelerate this substitution trend. Huawei's plans to double chipmaking capacity this year, and Cambricon's target to triple production, signal that Chinese supply is scaling to meet the structural demand.

A further structural advantage, and one that is frequently underappreciated by global investors, lies in the depth and sophistication of China's manufacturing ecosystem, built over decades of industrial development. In the fast-growing humanoid robotics space, Nvidia CEO Jensen Huang has described China as "formidable," citing the country's world-class microelectronics, motors, rare earth materials, and magnets as foundational inputs for robotics that China commands at unrivalled scale and quality. Chinese component suppliers have become indispensable to Tesla's 'Optimus Chain,' effectively supplying all critical subsystems of the humanoid robot, including actuators, motors, reducers, and vision systems, in a structure reminiscent of Apple's iPhone supply chain. While final assembly is slated for the US, the core component supply chain is anchored in China. Morgan Stanley estimates that removing Chinese components from the Optimus Generation 2 would push unit costs from $46,000 to $131,000, nearly tripling the price tag.

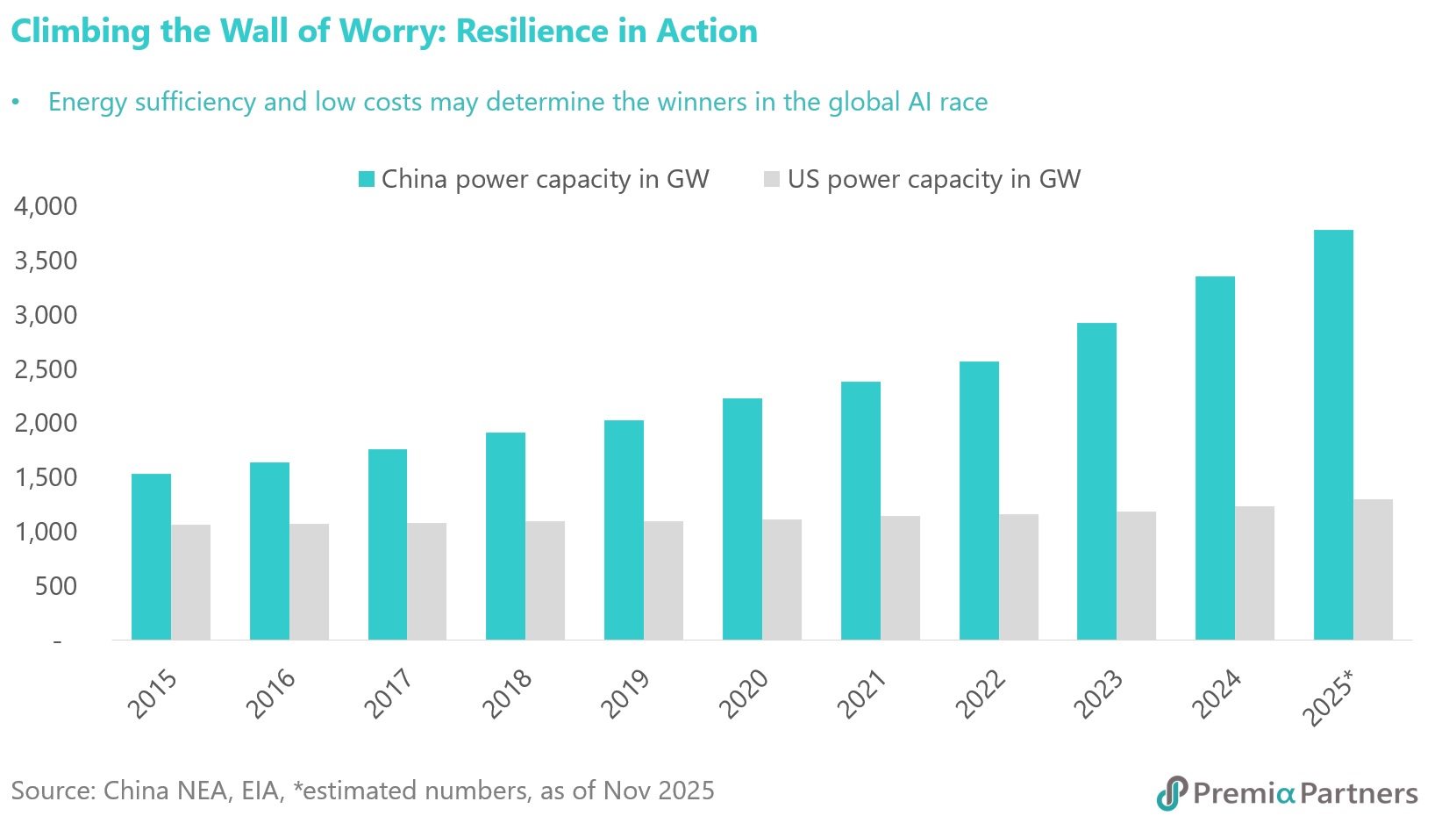

In the age of AI, electricity has become the new "fuel" of computation. Training and running frontier AI models demands enormous, sustained power, often on a scale comparable to small cities. Increasingly, the binding constraint on AI development is no longer the algorithm or even the chip, but rather power sufficiency, grid stability, and energy cost. This is where China's infrastructure advantage shines. China has more than doubled its installed power capacity over the past decade, while US capacity has grown only marginally over the same period, creating a widening structural gap in the energy headroom available to support large-scale AI infrastructure buildout.

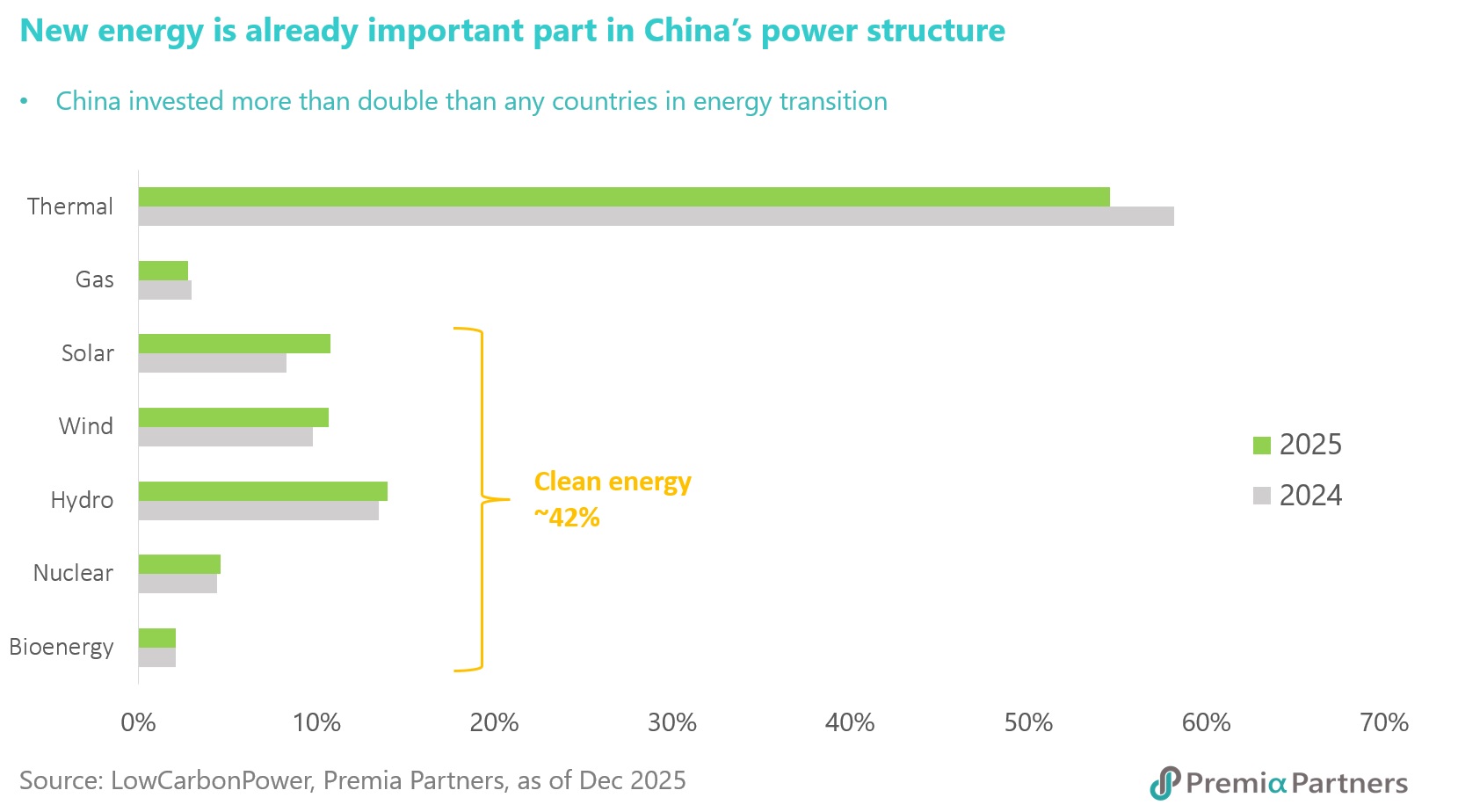

The composition of China’s capacity additions is also changing the cost equation. The majority of new generation capacity is coming from renewables, wind and solar, which benefit from declining long-run costs and reduce China’s dependence on energy imports. Strategic co-location of data centers with renewable energy bases, combined with an ultra-high voltage transmission network, further enhances the efficiency of the system. Looking ahead, China has committed approximately RMB 5 trillion in grid investment over the next five years to construct a national supergrid, an initiative designed to ensure that remote renewable generation can be efficiently transported to the data-intensive coastal and industrial hubs where AI computation is concentrated.

Meanwhile as countries are managing oil price hike and shortages amid the Hormuz crisis, China as the world’s largest net importer of oil and gas, and the biggest user of the Strait of Hormuz, is uniquely insulated after years of persistent efforts in diversifying its energy mix. This resilience is providing China with unique advantage vis a vis other major exporting countries.

In addition to the massive strategic petroleum reserve capable of covering over 100 days of net imports, oil and natural gas account for only a fraction of China’s total energy consumption, and according to Nomura Chief China Economist Lu Ting, “the share directly reliant on imports through the Strait of Hormuz is roughly 6.6% for crude and 0.6% for gas”. Meanwhile with abundant domestic reserves of coal, it remains important backbone for stable, low-cost, uninterrupted electricity supply in China which is crucial not only for AI but also for advanced manufacturing. While analysts estimate natural gas and oil account for 3.2% and less than 1% of China’s electricity generation, most other major manufacturing markets are much more exposed with between 30-70% of their electricity generation reliant on gas and LNG. In addition to short term cost advantages, the oil crisis also exposed the flaw of decoupling from China supply chain given its resilience and cost and scale advantage through not only industrial automation, but also diversified energy sources and technology-enabled energy infrastructure.

Several market tailwinds are also converging to support further outperformance of China tech equities in the onshore market.

- At the stock level, consensus earnings estimates for STAR50 Index and China New Economy Index constituents are being revised upward, a positive signal reflecting improving fundamental momentum. At the market level, Goldman Sachs recently upgraded its 2025 earnings growth forecast for China A-shares from 8% to 10%, and projects 13% growth for 2026 among the more constructive outlooks in global emerging markets.

- On the policy front, China remains firmly in an easing cycle, with monetary stimulus through liquidity injections and targeted fiscal incentives channeled into strategic tech sectors. Policy and growth are now pulling in the same direction, a stark contrast to the regulatory headwinds that weighed on China equities in prior years.

- Valuation is attractive: China A-shares trade at a forward P/E of approximately 13.4x, a material discount to global equities at 17.1x, offering institutional investors an attractive entry point into a structurally improving earnings story. International investors, currently underweight China in their portfolios, may increasingly recognize the diversification value of China tech as a source of growth uncorrelated with crowded US technology exposures. Domestically, persistently low deposit rates and bond yields are sustaining a structural rotation of household savings into onshore equities.

- The renminbi adds a further dimension: non-deliverable forward markets are pricing in approximately 2.2% appreciation over the next twelve months, which would potentially enhance total returns for foreign investors in USD terms while simultaneously signaling policy confidence, attracting capital inflows and supporting domestic consumption.

In summary, the combination of strong policy support, accelerating domestic substitution, a world-class manufacturing base, and expanding energy infrastructure, alongside improving earnings and attractive valuations, makes China tech one of the most well-supported opportunities in global equities today. For investors seeking focused exposure to China's leading hardcore technology companies, our Premia China STAR50 ETF offers a direct and efficient way to position for this theme including emerging hard tech sectors such as quantum and space technologies which are missing from mainstream mega-cap focused strategies. For those preferring broader participation across close to 300 holdings spanning industrial automation, advanced materials, clean energy, and biotechnology, our Premia CSI Caixin China New Economy ETF provides comprehensive coverage of China's new economy transformation.