Premia 圖說

Earnings momentum and growth expectations driving investor flows in China - Jun 15, 2026

賴子健 , CFA

CFA

China A-share market has become increasingly polarized, as earnings momentum and growth expectations drove investor flows. While the Information Technology sector has surged 31.9% year-to-date, Consumer Staples have declined 13.8%, illustrating a clear market preference for growth-oriented industries over traditional defensives. The strength of the technology sector is often attributed to the global enthusiasm surrounding artificial intelligence and semiconductor demand, alongside Beijing’s continued support for domestic innovation and import substitution in critical technologies. However, the rally is far from being purely sentiment driven. Corporate fundamentals have provided substantial support. In the first quarter of 2026, Information Technology companies delivered earnings growth of 68.0% year-on-year, second only to Materials at 74.8%. In contrast, Consumer Staples reported a 15.4% earnings decline, reflecting weaker operating momentum. The earnings divergence has also been reinforced by analyst revisions, with full-year profit estimates for Information Technology revised upward by 7.4%, while Consumer Staples experienced a sharp 19.3% downgrade. Looking ahead, earnings growth is expected to remain concentrated in a handful of high-growth sectors. Consensus forecasts point to full-year 2026 earnings growth of 72.0% for Materials, 70.6% for Information Technology, 33.7% for Industrials, and 30.8% for Healthcare, while Utilities, Financials and Consumer Staples are expected to lag. For investors seeking exposure to China’s structural growth themes, the Premia China STAR50 ETF and Premia China New Economy ETF offer targeted access to innovative and high-growth segments of the market, both of which have outperformed the broader A-share market year-to-date.

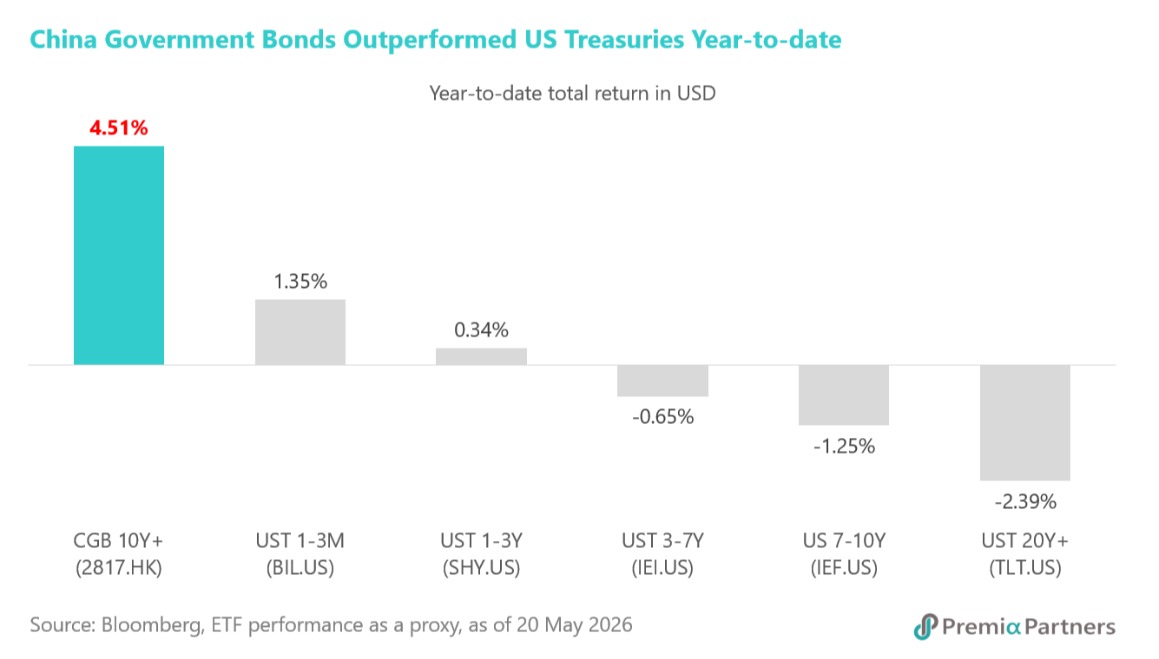

CGBs remain as haven assets - May 28, 2026

賴子健 , CFA

CFA

China government bonds have quietly emerged as one of the strongest-performing major sovereign bond markets year-to-date, standing in sharp contrast to the losses seen across most developed and emerging market fixed-income assets. While elevated crude oil prices and geopolitical tensions have reignited global inflation concerns, bond markets in the US, Europe, Japan, and several emerging economies have come under pressure as investors increasingly price in the risk of further policy tightening. US Treasury yields, in particular, have risen sharply amid growing expectations that the Federal Reserve may need to resume rate hikes by the end of this year, with other central banks potentially following suit to contain inflationary pressures. China, however, presents a very different macro and policy backdrop. While expectations for near-term rate cuts by the People’s Bank of China have faded alongside improving domestic growth, policymakers are likewise not expected to move toward tightening. The PBOC continues to maintain a supportive and “moderately loose” policy stance, while China’s inflation pressures remain relatively contained. This divergence has reinforced the defensive characteristics of China government and policy bank bonds, which continue to provide stability and steady returns while many global bond markets face ongoing capital loss risks. For institutional investors seeking duration exposure with lower inflation sensitivity and reduced tightening risk, the Premia China Treasury and Policy Bank Bond Long Duration ETF offers efficient access to one of the few major sovereign bond markets still benefiting from a supportive monetary environment.

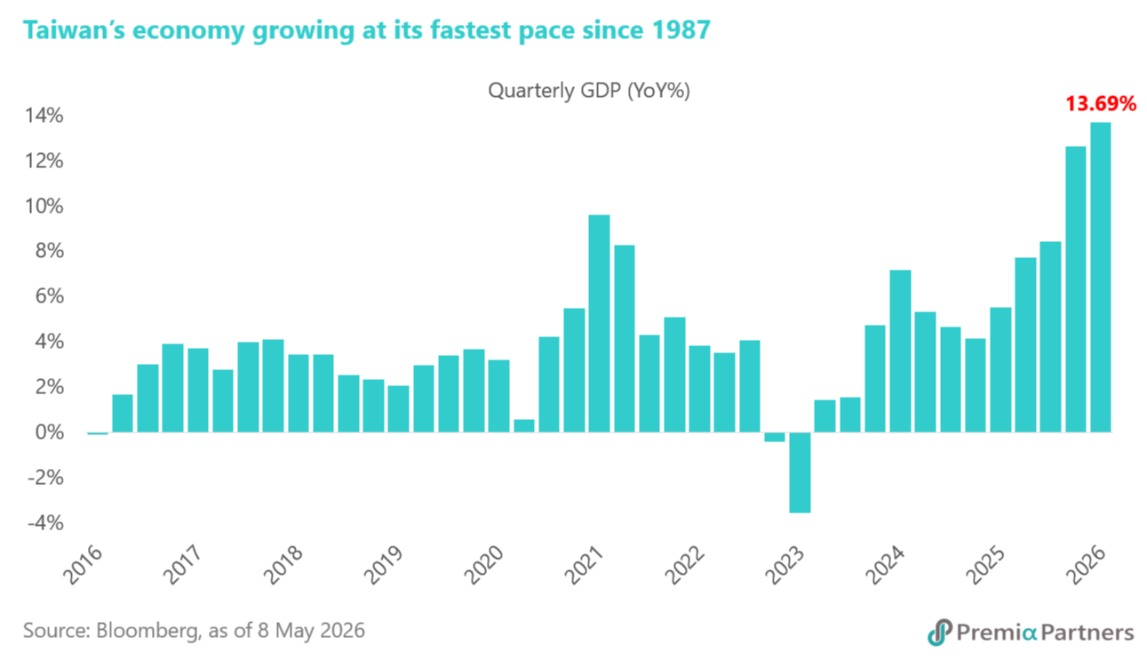

Taiwan's Q1 GDP growth reached 13.69% amid the global AI boom - May 11, 2026

賴子健 , CFA

CFA

Taiwan’s economy continues to demonstrate exceptional strength, supported by its increasingly indispensable role in the global AI supply chain. First-quarter GDP expanded 13.69% year-on-year, marking the fastest pace of growth since 1987. The upside surprise was driven primarily by robust external demand, as exports surged on the back of accelerating global investment in AI infrastructure, semiconductors, and high-performance computing. Electronic components and ICT products accounted for nearly 80% of total outbound shipments, reinforcing Taiwan’s position at the center of next-generation technology manufacturing. The strength of the export cycle is also translating into broader domestic economic momentum. Technology companies continue to expand capacity and increase R&D spending to capture long-term AI opportunities, supporting manufacturing activity and capital formation. Meanwhile, buoyant equity market turnover and increased participation in investment products have provided an additional tailwind for Taiwan’s financial sector. With global AI capital expenditure expected to maintain a strong multi-year growth trajectory through the end of the decade, Taiwan remains structurally well-positioned to benefit from rising demand across the semiconductor and advanced electronics ecosystem. Against this backdrop, Taiwan equities should continue to enjoy strong medium-term earnings support and investor interest. For investors seeking efficient exposure to Taiwan’s leading technology champions, including TSMC, MediaTek, Delta Electronics, and ASE Technology, the Premia FTSE TWSE Taiwan 50 ETF offers a focused and liquid vehicle to access Taiwan’s AI-driven growth story.

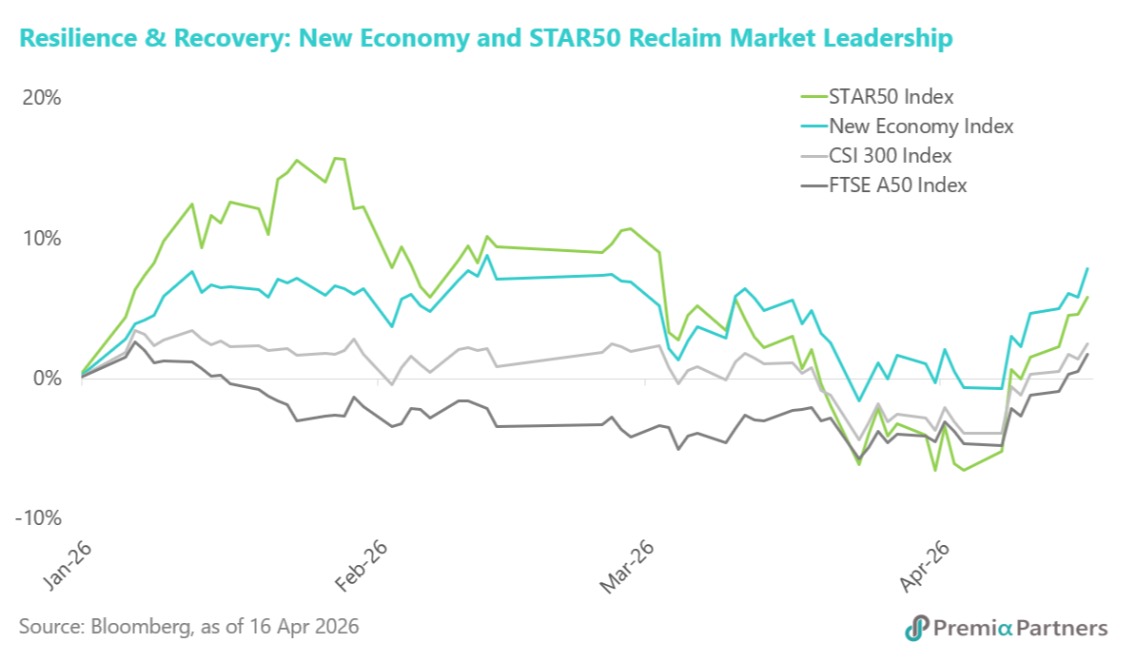

China hardcore tech and growth stocks outperforming - Apr 20, 2026

朱榮熙

Chinese new economy stocks, led by battery and semiconductor names, have reclaimed the outperformance against the broader market year-to-date, shrugging off ongoing US-Iran geopolitical noise. This resilience is underpinned by a combination of macroeconomic reflation, structural policy support, and accelerated technological self-reliance. On the macro front, China has officially exited factory deflation after more than three years. This is a critical inflection point: Goldman Sachs research shows that equities perform best when growth stabilizes alongside steadily rising inflation, with a concurrent PPI rate in the 0-4% range generating the highest historical returns across 1- to 12-month horizons. This reflationary tailwind is being amplified by targeted sector developments. In the battery and renewable space, the government summoned 16 leading manufacturers to restrict unchecked capacity expansion and curb price wars. Furthermore, the NDR’s new Order No. 41 raises thresholds for energy storage stations. Together, these moves force the industry to transition from “scale expansion” to “high-quality development”, directly benefiting top-tier power equipment and ESS producers. Simultaneously, the push for semiconductor self-reliance is accelerating. Reports indicate that DeepSeek’s highly anticipated V4 model will run on Huawei AI chips instead of Nvidia GPUs–a massive endorsement of domestic AI infrastructure that sparked a rally in local names like Cambricon. Should this reflationary momentum continue, new economy stocks are positioned to widen their outperformance gap. Investors forced on upstream hardware can capture this through our Premia China STAR50 ETF. For a broader play on this innovative growth story–spanning semiconductors, AI, EVs, and biotech–our Premia CSI Caixin China New Economy ETF offers an optimal, diversified approach.

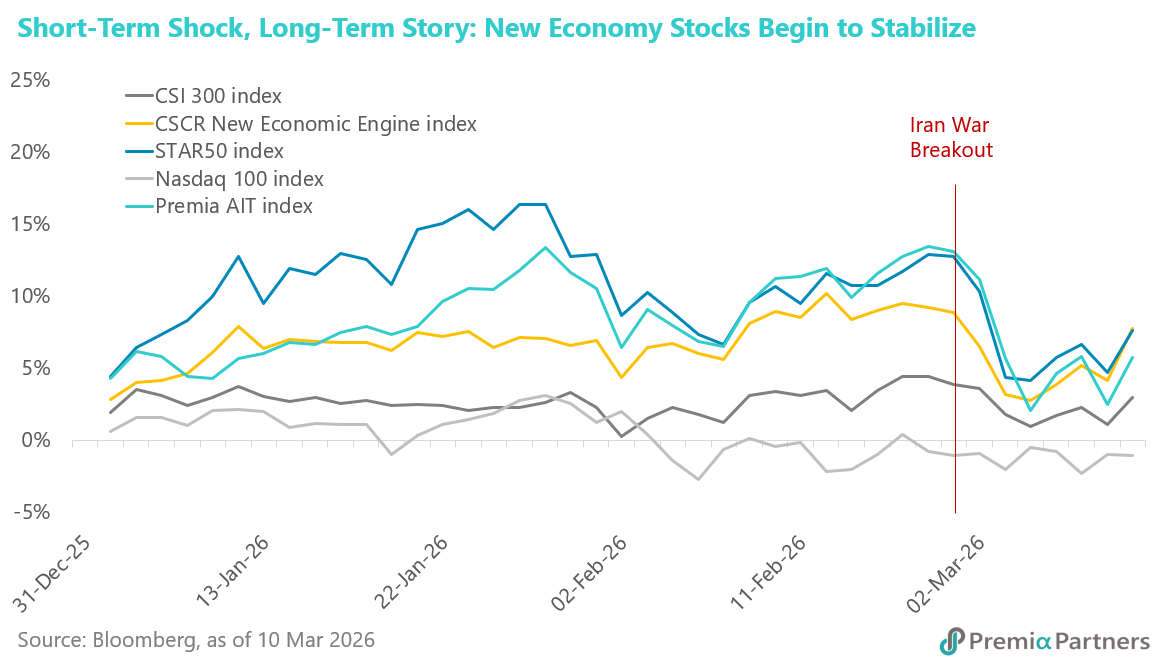

Time to accumulate China and Asia growth stocks - Mar 16, 2026

朱榮熙

While Chinese new economy stocks have faced short-term volatility amid the geopolitical tensions, their long-term growth remains anchored by strategic policy and industry breakthroughs. The 15th Five Year Plan underlines that technology and self-sufficiency still come first, backed by a strong push for AI and digital infrastructure. The blueprint mentioned "AI" more than 50 times and included major action plans to deploy AI agents and increase investment in quantum computing and 6G. On the hardware front, sources indicate SMIC (688981 CH) and other Huawei-linked chipmakers are aiming to ramp up production of 7nm or 5nm semiconductors to 100K wafers in 1-2 years to support domestic developers. This domestic ecosystem is already bearing fruit: Zhipu AI released its GLM-5 model with superior coding capabilities, notably confirming the model was developed using domestic chips from Huawei, Moore Threads, and Cambricon. On the software side, adoption is accelerating. OpenClaw has sparked a new trend pivoting from “Chat AI” to “Execution AI”, reminding investors of the DeepSeek moment in 2022. Chinese AI companies act swiftly to adopt the trend, making China a leader in consumer AI adoption. Multiple developers like Tencent and Xiaomi are linking OpenClaw to their models. Even before this new trend, local media have reported that Chinese AI models’ weekly token usage surpassed US peers, suggesting that monetization may arrive earlier than expected. Investors focused on hardware semiconductors could consider our Premia China STAR50 ETF. For broader exposure, our Premia CSI Caixin China New Economy ETF offers a diversified approach with investments in semiconductors, AI, EV, and Biotech, allowing investors to participate in China’s innovative growth story. For even broader Asia exposure, investors might consider our Premia Asia Innovative Technology and Metaverse Theme ETF, which invests in Asia's 50 largest innovative companies across sectors such as AI, semiconductors, solar energy, and EVs with equal weightings.

Taiwan equities going from strength to strength - Feb 23, 2026

賴子健 , CFA

CFA

Taiwan's economic outlook is experiencing a significant uplift, driven by the burgeoning AI revolution and a recently cemented trade pact with the US. Economic growth forecasts for this year have been upgraded to an impressive 7.7%, a substantial increase from the 3.5% projection made in November. This revised outlook anticipates Taiwan's GDP reaching an unprecedented USD1tn, marking a historic achievement for the island. Fueling this robust growth is an expected surge in exports, now projected to rise by 22.2% in 2026, a sharp acceleration from the earlier 6.3% forecast. These positive revisions reflect a broad consensus among financial institutions, with Bank of America nearly doubling its growth prediction due to "relentless global demand" for Taiwan's advanced tech hardware, including critical AI chips and servers. The enhanced capital expenditures by cloud providers, exceeding initial expectations, further underscore the formidable strength of AI-related infrastructure. The strategic trade agreement finalized between the US and Taiwan earlier this month is a pivotal catalyst, set to reduce average tariff rates on Taiwanese exports to the US from nearly 36% to ~12%. This landmark deal, hailed as a shift from "defense to offense" by Taiwan Premier Cho Jung-tai, will cement Taiwan’s position as an economic powerhouse. The tangible impact of these developments is already visible in Taiwan's equities market, which has seen remarkable performance. The stock market has advanced by at least 25% for three consecutive years, with a further ~15% gain to a new record in 2026 alone. For institutional investors looking to capitalize on this strong structural uptrend in Taiwan equities, the Premia FTSE TWSE Taiwan 50 ETF presents an optimal and strategic investment vehicle to capture this solid growth story.

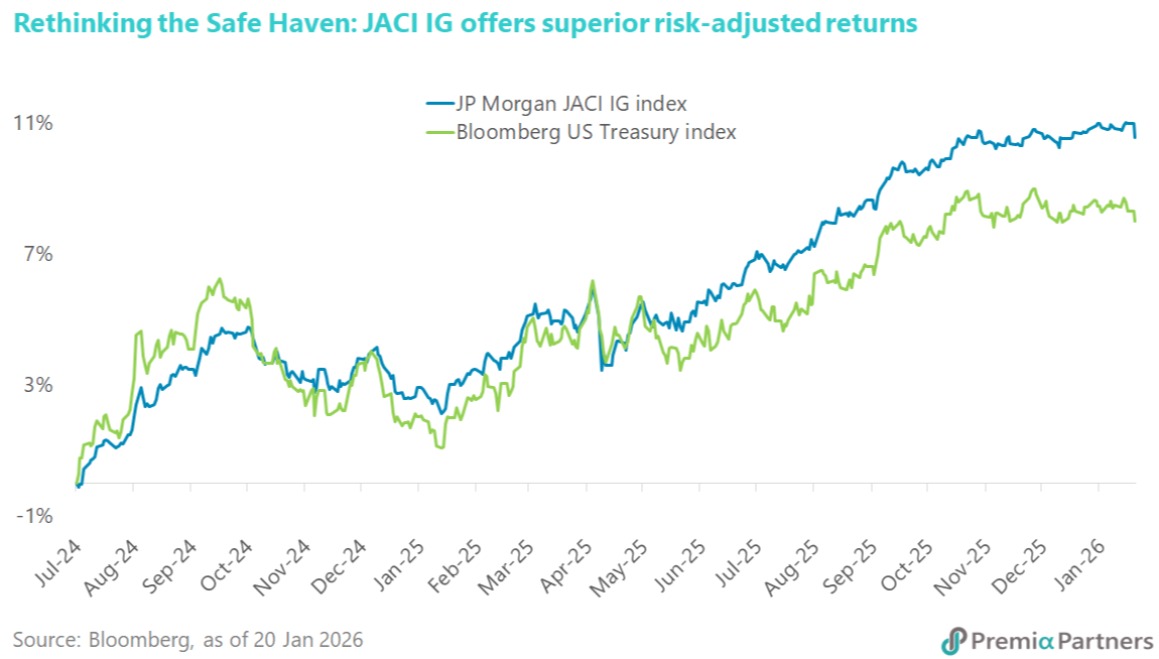

Rethinking the safe haven - Jan 28, 2026

朱榮熙

The immediate threat of a US-EU trade war has subsided with President Trump’s sudden reversal on tariffs, but the underlying tensions remain unresolved. Denmark has already denied the existence of any deal to cede Greenland, suggesting this reprieve may be temporary. This constant policy whiplash reinforces the view of major institutional investors like AkademikerPension that US Treasuries are increasingly fraught with headline risk. As their CIO notes, the 'massive credit risk' posed by US governance issues means investors must look beyond the immediate news cycle and plan for a future where US assets are no longer the sole definition of safety. This environment validates the case for Asia Investment Grade (IG) as a superior alternative. The asset class is not only shielded from Western political brinkmanship but is also undergoing a positive transformation. We are seeing a healthy diversification in issuers, highlighted by Kuaishou Technology entering the market to fund its AI ambitions. This signals that Asia IG is evolving from traditional sectors into a dynamic, tech-forward asset class. For investors seeking stability without sacrificing growth, the Premia J.P. Morgan Asia Credit Investment Grade Bond ETF offers diversified exposure to these solid sovereign and corporate credits, serving as a prudent hedge against the unpredictable winds of Washington."

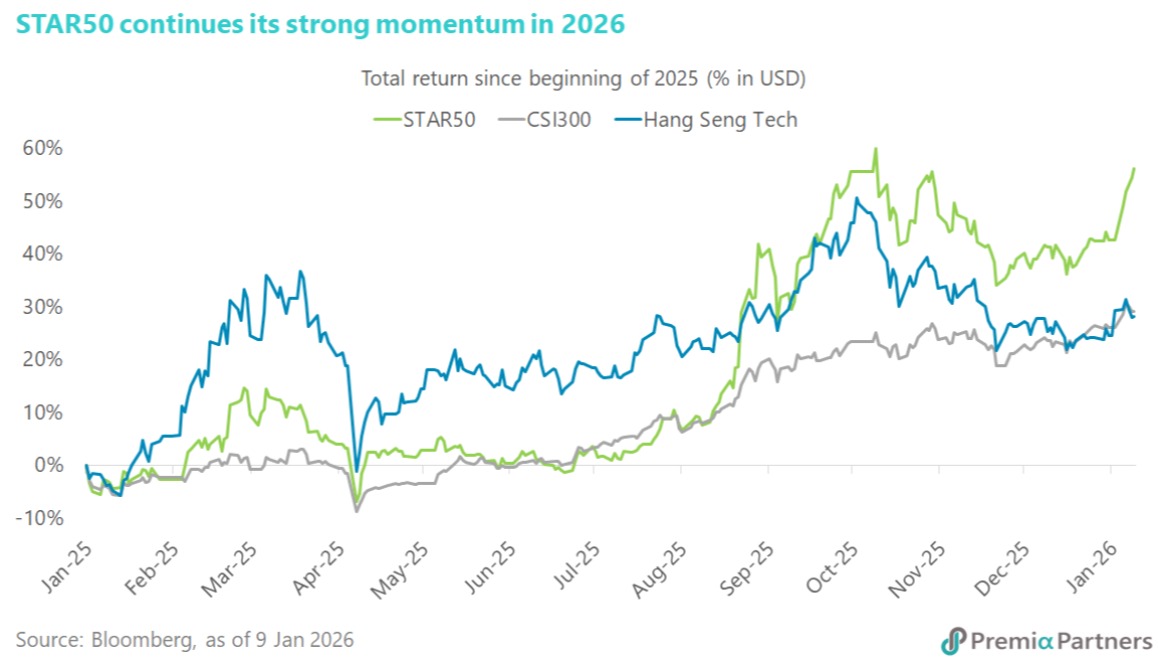

STAR50 going strength to strength in 2026 - Jan 12, 2026

賴子健 , CFA

CFA

Chinese equities got off to a strong start in 2026, led by the STAR Market. Since onshore trading resumed, the STAR50 Index has risen 9.9% in dollar return, outperforming CSI300’s 2.9% and offshore Hang Seng Tech’s 3%. This extends the strong momentum seen in 2025, when the STAR50 delivered a dollar return of 42.6%, well ahead of CSI300’s 26.3% and Hang Seng Tech’s 24.5%. Policy signals remain supportive. In his New Year’s Eve address, President Xi highlighted China’s progress in artificial intelligence and semiconductors, reinforcing innovation as a core pillar of high-quality economic development. Advances in humanoid robotics, drones, aerospace, and defence were cited as key examples. At the corporate level, the China Integrated Circuit Industry Investment Fund (“Big Fund”) increased its stake in SMIC, the largest constituent of the STAR50 Index, from 4.79% to 9.25%, showing state support for advanced-node capabilities. Among the outperforming stocks, Guobo Electronics rose close to 40% over the past five trading days, following reports that China aims to scale up to 100 rocket launches annually by 2030. As a leading supplier of RF chips and T/R modules, Guobo is a major beneficiary of rising demand for satellite and launch-vehicle communications. AMEC shares also surged after announcing the acquisition of a 64.7% stake in Hangzhou Zhongsilicon, expanding its offering from dry processes into chemical mechanical polishing. Meanwhile, VeriSilicon Microelectronics reported a 130% year-on-year increase in new orders last quarter, driven by accelerating AI chip demand. Against this backdrop, the Premia China STAR50 ETF allows investors to align portfolios with China’s strategic push in advanced technology and innovation through the STAR Market.

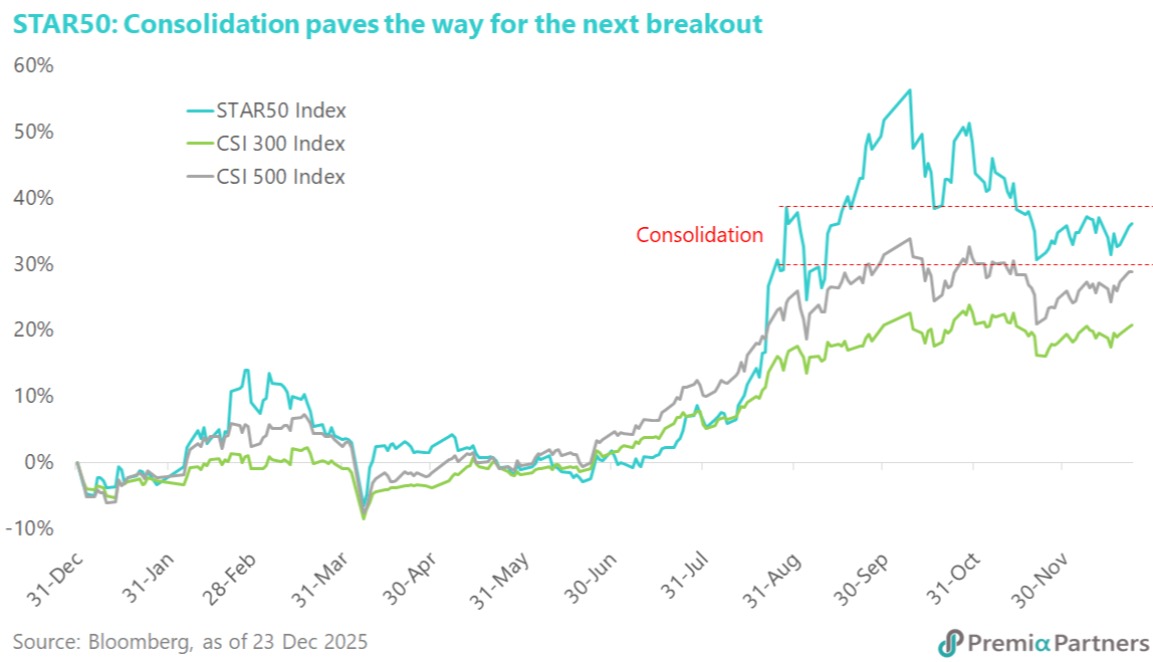

STAR50 - Consolidation paves the way for the next breakout - Dec 29, 2025

朱榮熙

China’s push for self-sufficiency in advanced manufacturing is showing no signs of slowing down as we approach year-end. Reuters report that China has completed a prototype EUV lithography machine, bypassing Western export controls, with working chip production targeted by 2028. Meanwhile, researchers at Shanghai Jiao Ton University have developed the world’s first all-optical computing chip capable of supporting large-scale generative models. This represents a paradigm shift beyond traditional silicon: by using photons instead of electrons, the chip eliminates heat resistance and allows data to travel at light speed—offering a critical solution to the energy and bandwidth bottlenecks currently facing global AI development. Extending the frontier further, the University of Science and Technology of China (USTC) achieved a critical milestone in quantum computing. Using the “Zuchongzhi 3.2” processor, the team made a breakthrough in quantum error correction; by suppressing errors below the critical threshold, they have validated a technical route for building future megabit-level quantum computers. Corporate innovation is equally robust. Moore Threads, which recently saw a 600% upside debut on the STAR Board, unveiled its 'Flower Harbor' GPU architecture, boasting a 10x improvement in energy efficiency. In robotics, Unitree’s G1 humanoid robot stunned audiences with a backflip—a feat Elon Musk called 'impressive.' As momentum builds in hard-tech sectors, the STAR Board is becoming an unmissable destination for growth. To capitalize on these opportunities, consider our Premia China STAR50 ETF, which offers direct exposure to these leaders with a market-leading capped expense ratio of just 0.58% p.a.

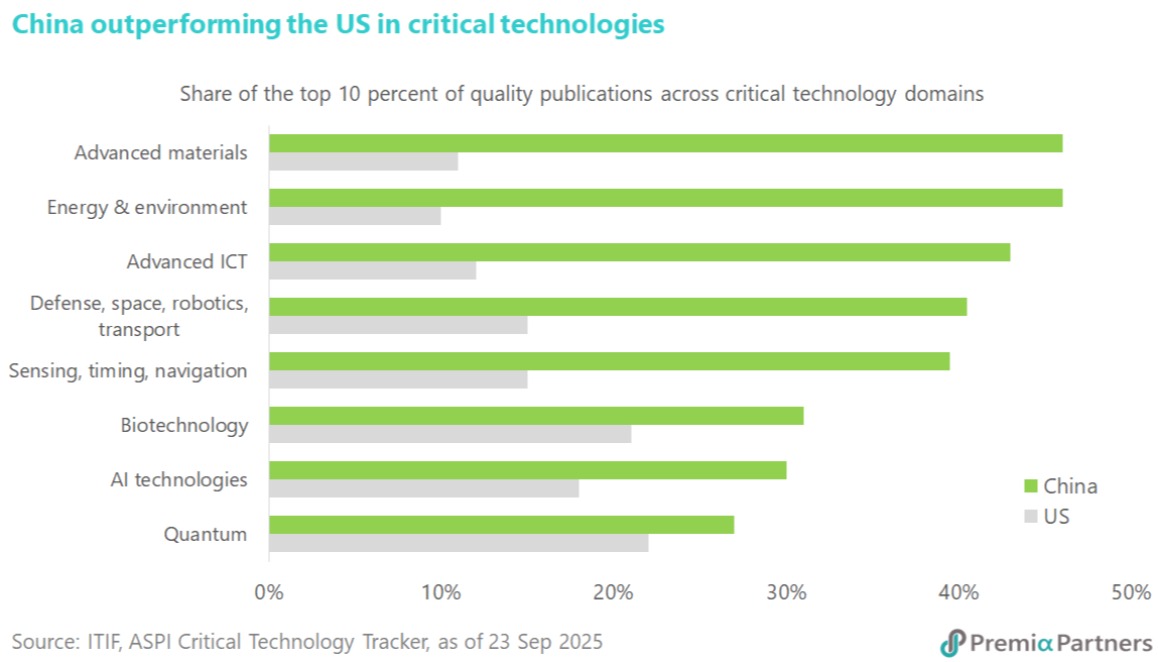

China building deep expertise across a wide range of frontier technologies - Dec 08, 2025

賴子健 , CFA

CFA

China’s rapidly advancing innovation ecosystem has positioned the country as a pivotal force in the global technology landscape. Its sustained commitment to research, strategic industrial policy, and talent development has enabled China to build deep expertise across a broad range of frontier technologies. Information Technology and Innovation Foundation (ITIF), a non-profit policy think tank based in Washington, D.C., highlights the scale of this progress. China now produces an increasingly large share of global scientific publications and patents, reflecting both the breadth and maturity of its research output. Momentum is particularly strong in high-growth areas such as robotics, advanced batteries, clinical biotech trials, quantum communication, artificial intelligence, advanced materials —fields where China’s state-supported infrastructure and robust innovation pipeline are translating into commercially meaningful breakthroughs. Further evidence from the Australian Strategic Policy Institute’s Critical Technology Tracker reinforces this trend. The analysis shows China holding a leadership position in the majority of the 64 critical technologies assessed, underscoring the effectiveness of its long-term investment in science, engineering, and education. China’s emphasis on STEM talent cultivation has created the world’s largest cohort of technical graduates, providing a deep and scalable foundation for continued innovation. These structural strengths—ranging from its research base to its industrial execution—collectively support a long runway of technological development and commercialization. For investors aiming to gain exposure to this accelerating innovation cycle, our Premia CSI Caixin China New Economy ETF and Premia China STAR50 ETF would be the essential tools.